AI-driven lending is fast, digital, and convenient—but are borrowers really aware of the hidden risks?

Interest rates that dynamically change without notice

Hidden processing & penalty fees buried in fine print

Arbitration clauses that block legal recourse

Auto-foreclosures triggered by AI risk models

In this article, I break down the risks, supported by data, real-life legal cases, and visual insights.

Have you ever faced unexpected charges in a digital loan? Let’s discuss—your experience could help others avoid financial pitfalls!

Loan agreements have always been full of fine print, but in today’s AI-driven lending world, risks are becoming more automated, less transparent, and harder to dispute. While AI makes financing faster, it can also amplify hidden risks for borrowers.

1. AI-Driven Interest Rate Adjustments

AI-powered lenders dynamically adjust interest rates based on real-time borrower data, but many borrowers are unaware that their rates can change unpredictably.

🔹 Example: A fintech lender increases interest rates for customers flagged as "risky", even if they have a clean repayment record.

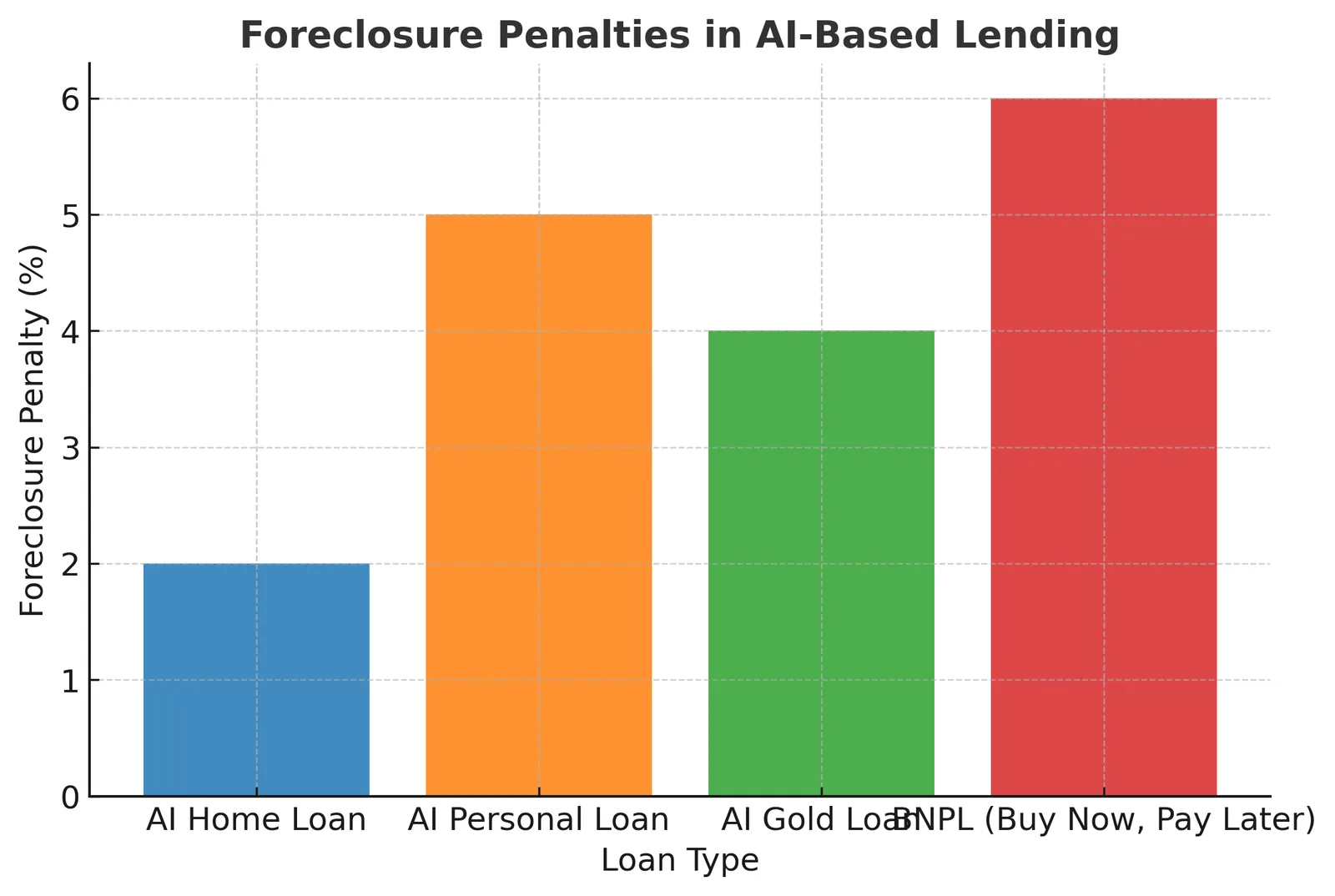

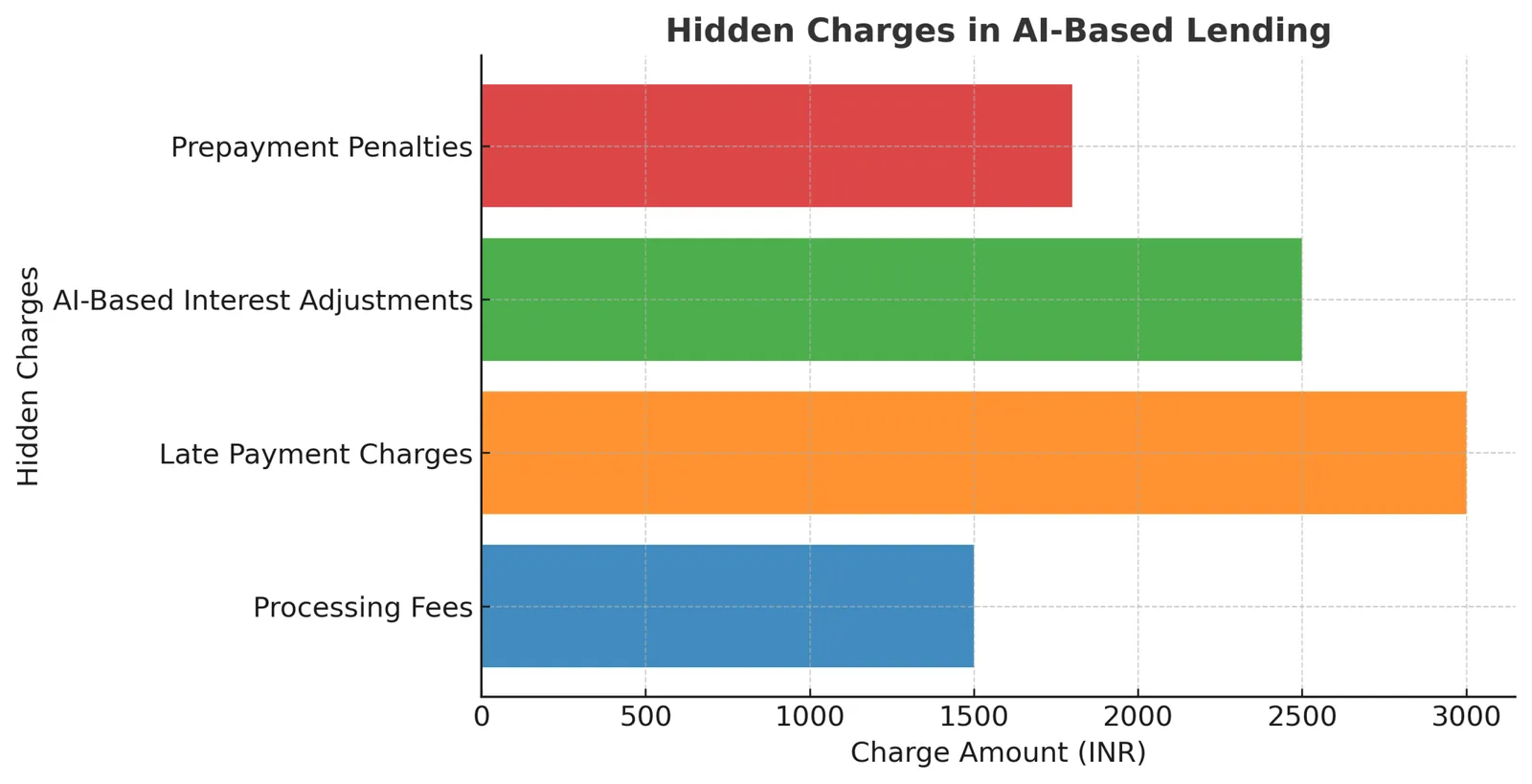

2. Hidden AI-Based Fees, Purchases & Automated Foreclosure

Many Buy Now, Pay Later (BNPL) schemes and AI-driven loans have hidden charges—processing fees, penalty interest, and auto-debit fines. Some AI systems automatically trigger foreclosure if repayment patterns change.

🔹 Example: In HDFC’s auto-loan case (2021), customers were forced to buy unnecessary GPS trackers. AI-driven fintechs now embed similar charges in digital loan contracts.

3. AI-Powered Gold Loan Schemes

Gold loans, once a straightforward process, are now influenced by AI-driven valuation algorithms. Many borrowers unknowingly pay hidden valuation, storage, and auction fees.

🔹 RBI’s 2024 investigation found that AI-driven lenders inflated hidden costs in gold loans.

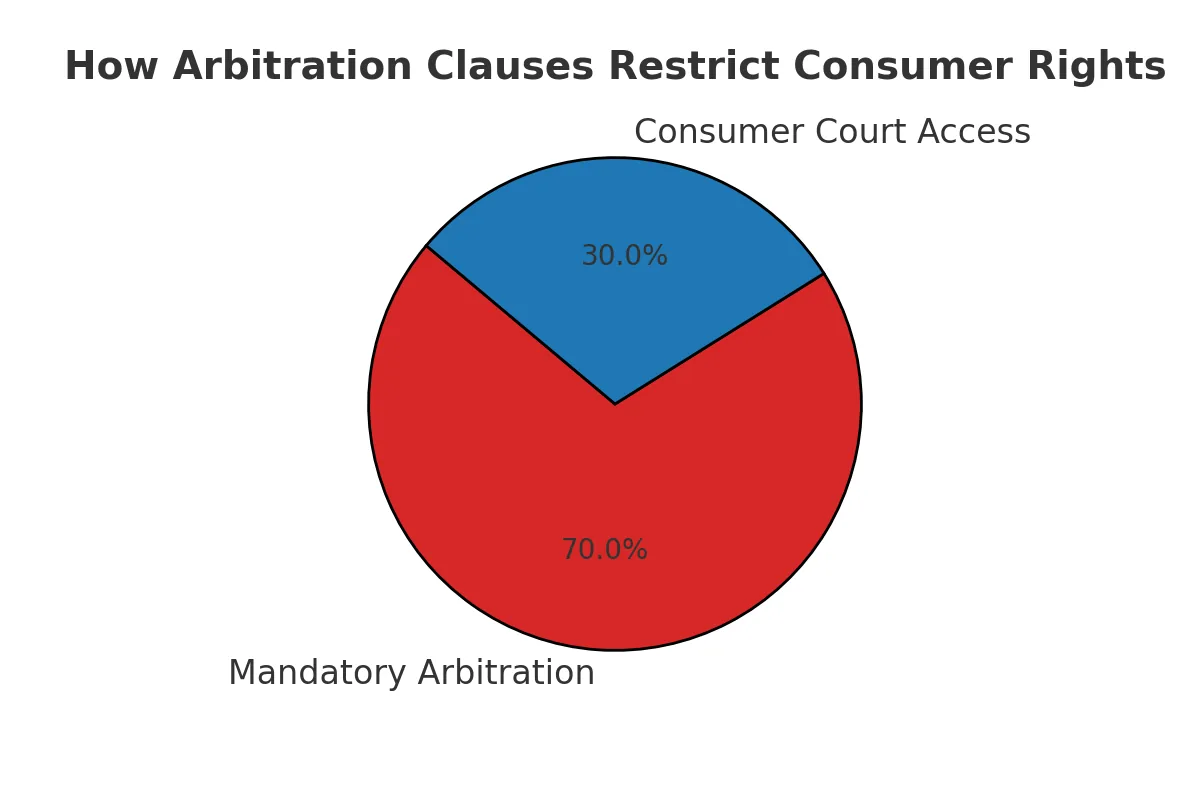

4. AI & Arbitration Clauses – The Hidden Legal Trap

Most digital lending agreements now include mandatory arbitration clauses, blocking borrowers from going to court. AI-based contract systems auto-approve such clauses, reducing consumer legal rights.

🚨 How to Protect Yourself 🚨

Always read digital loan agreements carefully.

Ask if interest rates are AI-adjusted & if there’s a cap.

Check if arbitration clauses restrict your legal rights.

Verify if AI-based lending decisions can be challenged manually.

In the AI-driven lending world, hidden risks are more automated and less transparent. Stay informed, question AI-based decisions, and demand full disclosure before signing any loan agreement.

👉 Have you faced hidden charges in digital lending? Share your experience! #Fintech #AIlending #FinancialAwareness #LoanRisks #Banking

This is just the beginning of a series of small write ups on the topic. These are jottings of CUG discussions with contributions coming in from various participants. Yet I found these engagements interesting and thought of breaking the discussions into smaller pieces for easier assimilation.

Disclaimer

"The views, opinions, and insights expressed in this article are solely my own and do not reflect those of my employer, organization, or any institution I am affiliated with. This content is intended for informational and educational purposes only and should not be considered as financial, legal, or professional advice. Readers are encouraged to conduct their own research and consult with relevant experts before making financial decisions."

Archive note

This essay was restored from Vivek Krishnan’s LinkedIn archive. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.