01

01Today’s Perspective

Three words. One connected view.

RebalancingCoordinationControl

Rebalancing moves credit toward segments where demand, pricing and risk appetite have changed. Coordination turns separate fraud reports and jurisdictions into a shared response. Control looks past a shareholding label to the rights and influence that shape decisions. Across all three desks, today’s lesson is to examine how resources, information and power are actually organised.

Read today’s full perspectivePlay · Entrepreneurappa

₹1,00,000. A ticking clock. One decision at a time.

Choose your licences, spend your opening cash and discover whether your business survives its first month.

Take the hot seat →Analyse · Bank AnalyzerGNPA fell from 4.50% to 3.20%. Is the new book seasoned enough?

A real South Indian Bank signal: the ratio improved, but the strategic question begins where the headline ends.

Interrogate the numbers →Test · Perspective LabWhat changes when two ideas are forced to meet?

Place two perspectives side by side. Find where they reinforce, contradict or reveal a third insight.

Find the hidden connection →Interactive

Don’t just read a perspective. Test one.

Put ideas under pressure—by comparing how two perspectives connect, or by making live business decisions with visible consequences.

Perspective Lab

Compare two ideas. Discover the connection.

Place two essays—or an essay and a reference—side by side and examine where they reinforce or challenge each other.

Enter the Perspective Lab →Entrepreneurappa · Live simulation

Can you build a business without losing the balance?

Start with ₹1,00,000, make setup and operating choices, and watch cash, time and risk respond.

Play Entrepreneurappa →New here? Start here

Three cornerstone choices.

A short route into the ideas, evidence and experience behind the site.

01 · Read

Begin with the newest episode

See how experience, evidence and AI connect in one practical lending argument.

Read the latest episode →02 · VerifyOpen the reference library

Move from an opinion to RBI material, bank reports, ACFE research and MSME schemes.

Explore references →03 · UnderstandMeet the practitioner behind it

Understand the three decades of banking, credit and transformation experience shaping these perspectives.

Meet Vivek →Connected series · 4 episodes

From Paperless Lending to Intelligent Lending.

A practical progression from digitising processes to building an explainable, sensing and continuously learning credit system.

Start at Episode 1 →4 of 4 published

Banking Risk Leadership AI

Seeing what the numbers don’t say.

Field-tested perspectives on credit, fraud, business, technology and the human decisions behind them.

Vivek Perspective is now live.Explore the complete essay library, guided reading paths and RBI references. The internal bank-report archive is opening progressively as verified documents are added.Enter the library →

Bank Analyzer

Compare the strategies of any 2 to 5 banks.

Examine growth, technology adoption, portfolio mix, strategic drivers, strengths, presence and key leadership.

Date-wise archives

Return to a perspective exactly as it appeared.

Browse each preserved Daily Edition by date, then return to the current day in one tap.

Browse Daily Edition archivesReading paths

Choose the question, not the format.

01

AI & Digital Lending

Technology examined through accountability, explainability and lived banking experience.

↗02Credit & Underwriting

Judgment-led underwriting, appraisal practice and questions worth asking.

↗03Fraud, Ethics & Governance

Patterns that reveal more than the paperwork—and the controls that should respond.

↗04Leadership & Reflection

Lessons from people, institutions, ordinary moments and the choices they illuminate.

↗05Tractor & Rural Finance

Where field realities, borrower intent and the economics of an asset meet.

↗From the library

Essays worth returning to.

AI & Digital Lending

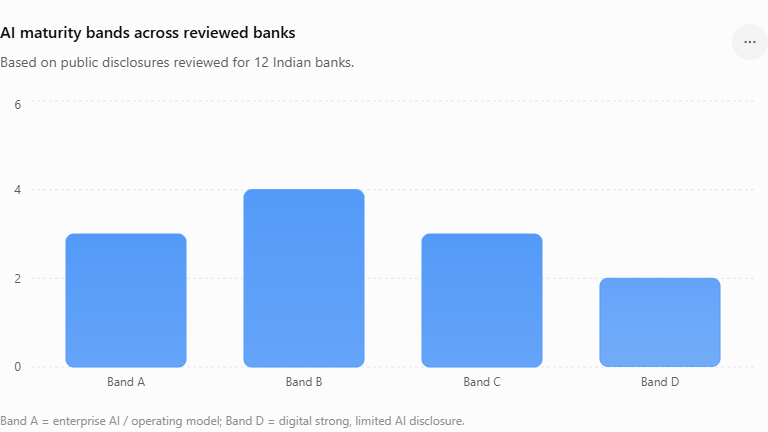

AI in Indian Banking: Hype, Reality and the Maturity Gap

A colleague asked whether AI adoption in banks really has depth. I paused to examine the public evidence. A colleague who had been reading my recent blogs on AI in lending called me with a simple question: “Is there really so much depth in AI adoption within banks, or are we overstating it?” It w…

AI & Digital Lending

From Paperless Lending to Intelligent Lending

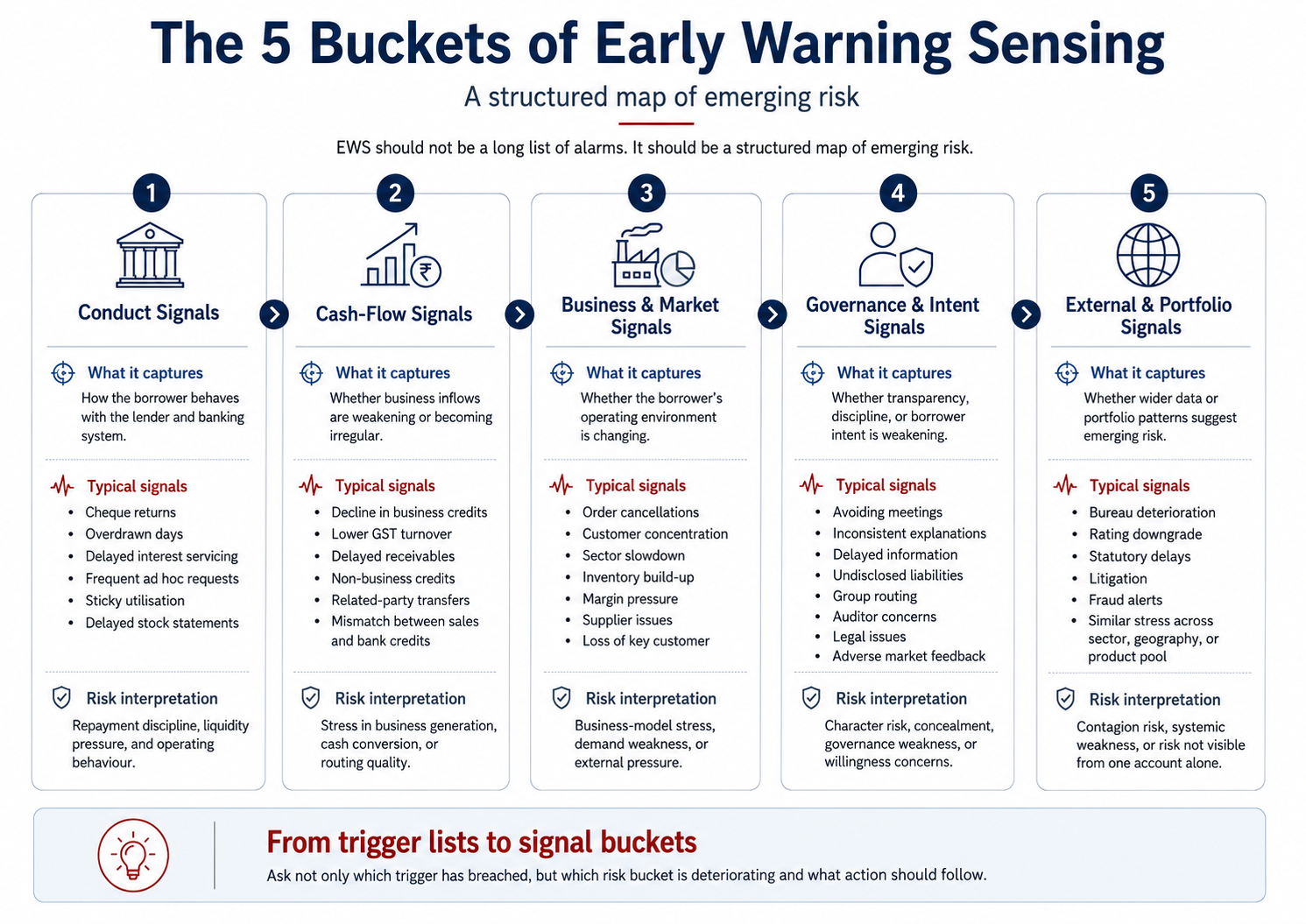

Early Warning Signals in lending must move beyond periodic reports and static triggers. Episode 4 of From Paperless Lending to Intelligent Lending explains how AI can help banks and NBFCs shift from EWS reports to early warning sensing by connecting conduct, cash-flow, business, governance and po…

AI & Digital Lending

From Paperless Lending to Intelligent Lending

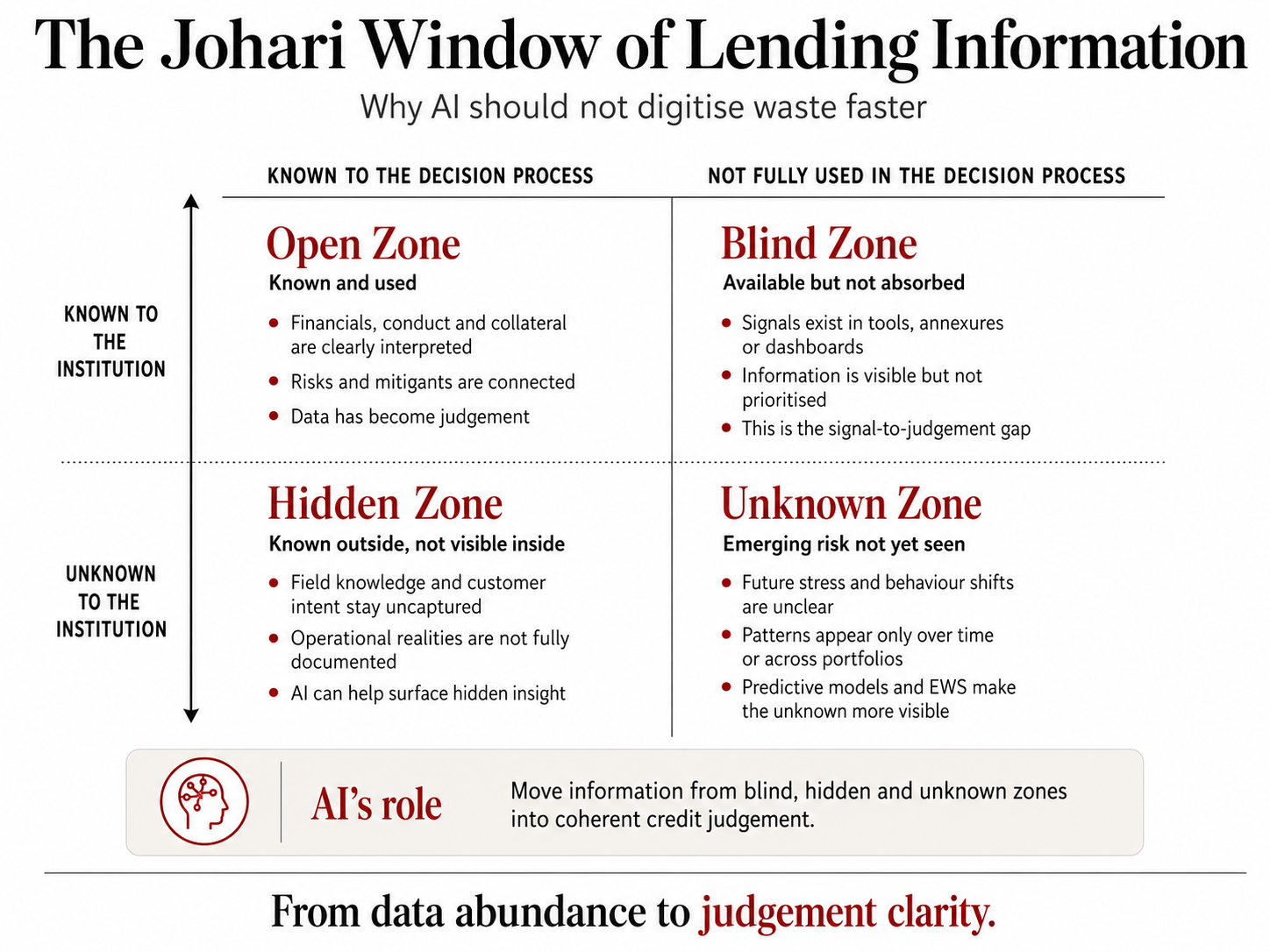

AI in lending should not digitise waste faster. Episode 3 of From Paperless Lending to Intelligent Lending uses the Johari Window to explain how banks and NBFCs can move from data abundance to judgement clarity. It explores signal platforms, the blind zone of unused analytics, the 40% signal wast…

AI & Digital Lending

From Paperless Lending to Intelligent Lending

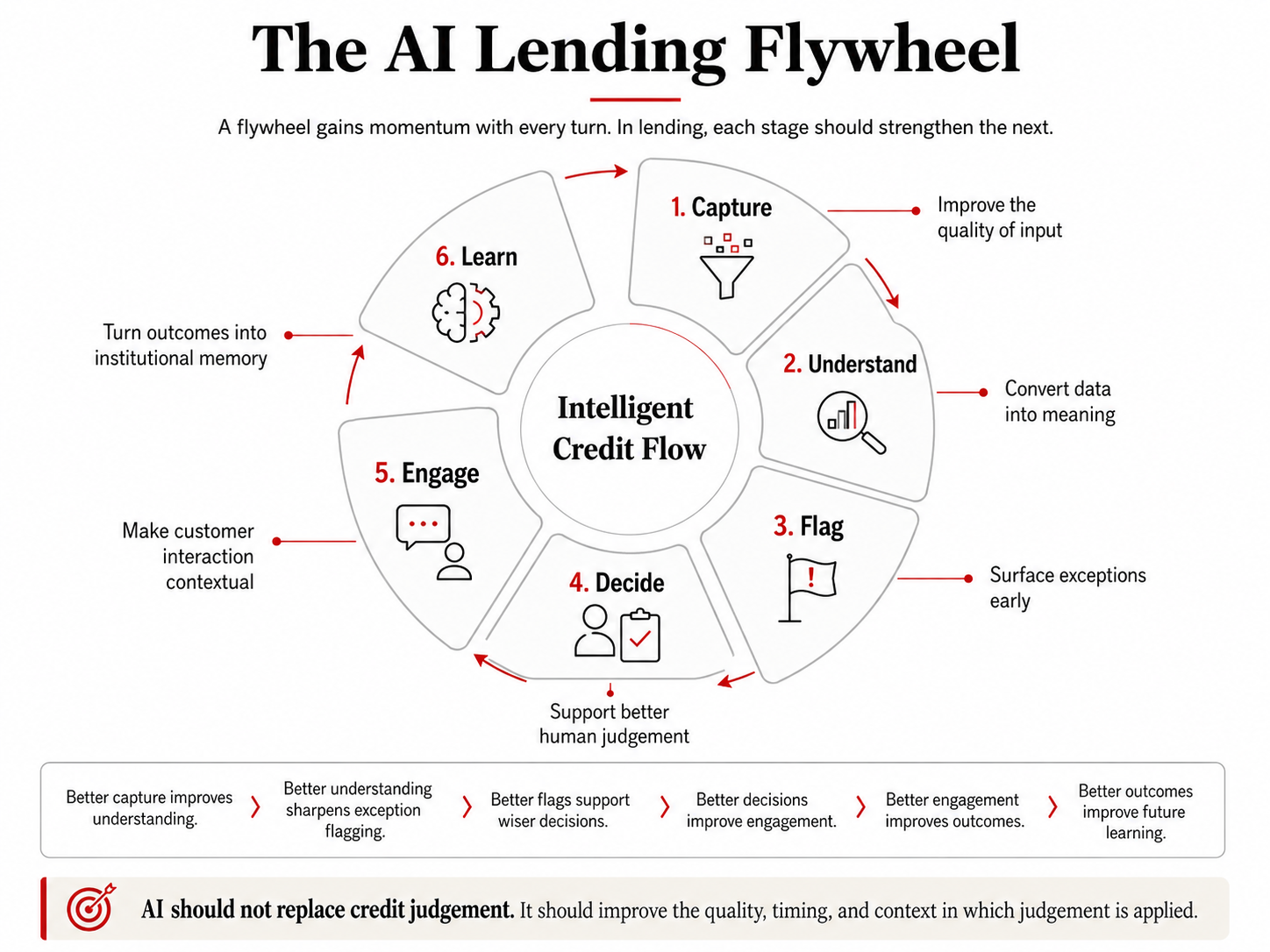

The AI Lending Flywheel explains how financial institutions can move from isolated AI pilots to intelligent credit flow. Built around six stages — capture, understand, flag, decide, engage and learn — the model shows how AI can improve the quality, timing and context of credit judgement without r…

AI & Digital Lending

From Paperless Lending to Intelligent Lending

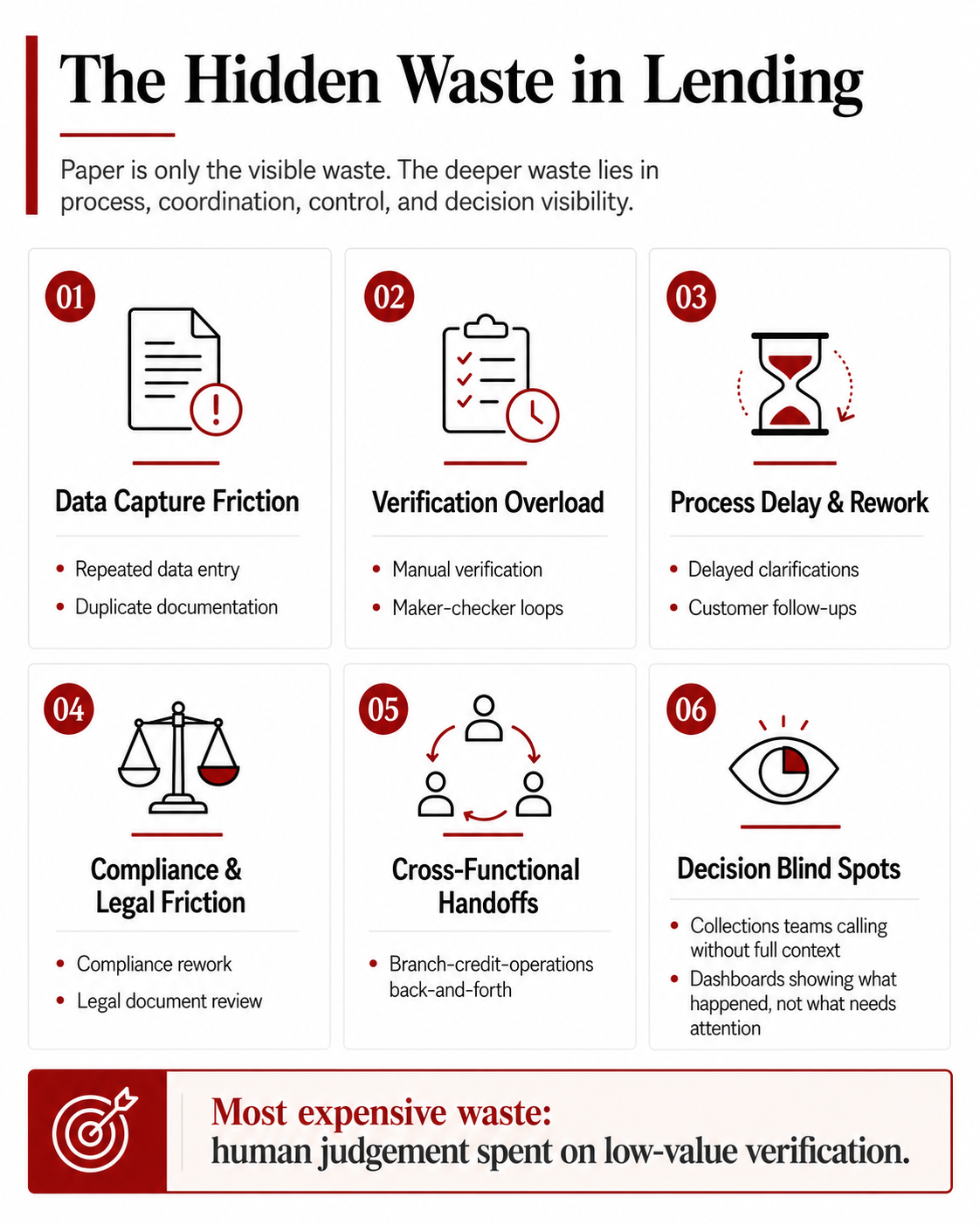

Paperless lending is only the first stage of transformation. The real opportunity lies in removing hidden waste in lending — waiting, rework, repeated checks, late exception discovery, dashboard noise and underused human judgement. This article uses a Lean lens to explain how AI can help move fin…

Fraud, Ethics & Governance

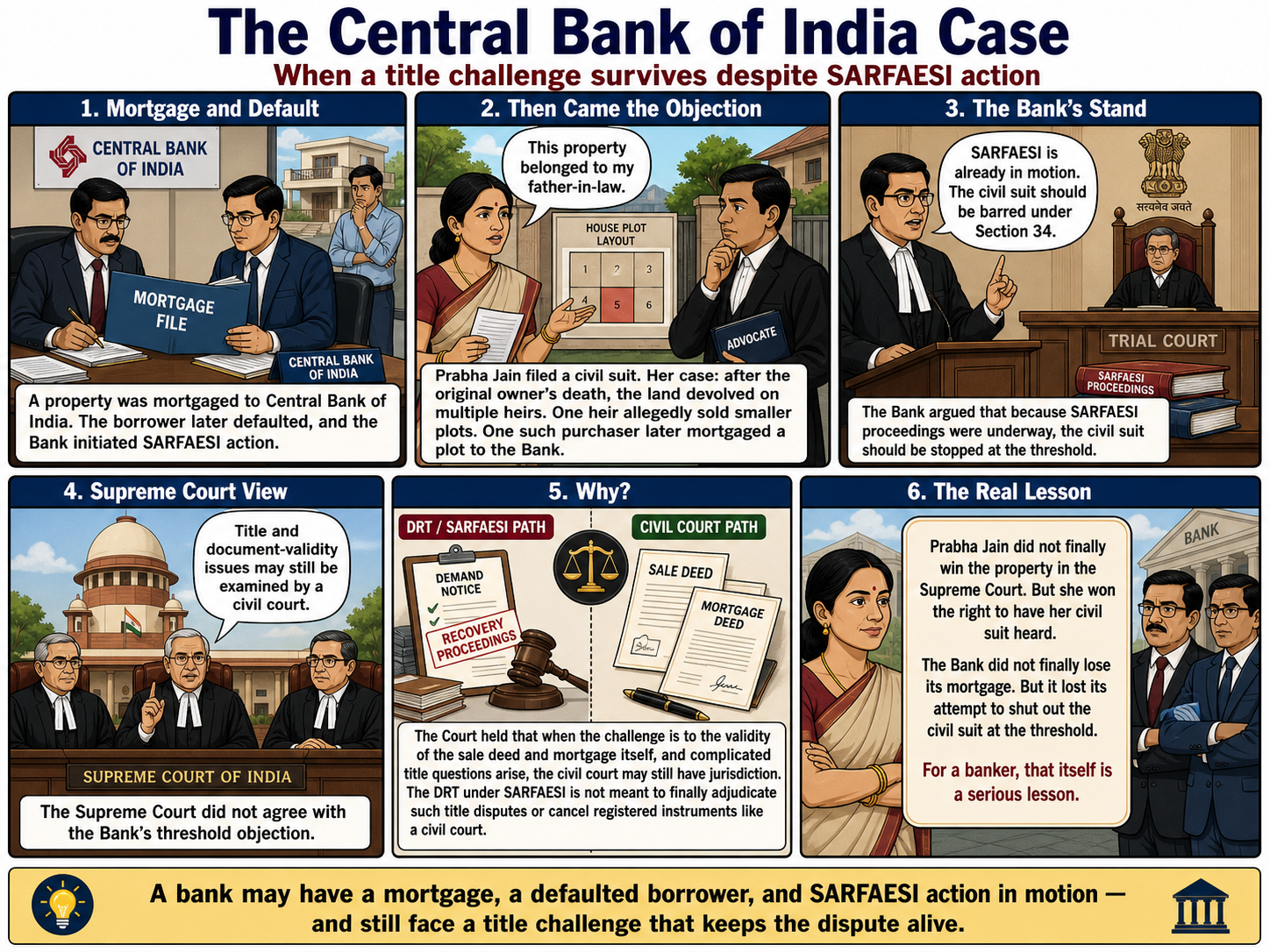

The Late Claim Trap: When Property Security Meets an Unanswered Title Challenge

A banker’s reflection on Central Bank of India v. Prabha Jain, 2025 INSC 95, where the Supreme Court held that a third-party challenge to sale deed and mortgage validity may still proceed before a civil court despite SARFAESI action. The case highlights the late claim trap, title litigation risk,…

Fresh perspective. Same discipline.Return tomorrow for a new perspective at 5:30 a.m. IST.Return to today’s perspective ↑