Episode 3 : Why AI should not digitize waste faster The Johari Window of Lending Information There is a danger in the current excitement around AI in lending. The danger is not that AI will be used. The danger is that AI may be used too quickly, too superficially and too proudly on processes that were never properly redesigned. If a process has repeated data entry, AI can make the repetition faster. If a Credit Assessment Memo has weak structure, AI can make the weak structure look polished. If dashboards only show what happened, AI can make the mirror more colourful without turning it into a radar.

If collections teams contact borrowers without context, AI can increase contact intensity without improving borrower understanding. If analytical tools generate dozens of signals but the credit process does not know how to interpret them, AI may create more analytical clutter. That is not transformation. That is digitising waste faster. The question for lenders is therefore not: Where can we use AI?

The better question is: Which waste, blindness or judgement gap are we trying to remove? The Information Problem in Modern Lending For a long time, lending suffered from lack of organised information. Financials came late. Bank statements were manually reviewed. GST information had to be separately obtained. MCA information was not easily organised. Bureau reports needed interpretation. Field feedback often stayed informal. Collections conversations rarely flowed back into credit thinking. That world has changed.

Today, lenders have access to bank statement analysers, GST analysers, bureau tools, MCA extractors, fraud checks, legal search tools, financial spreading tools, dashboards and risk-intelligence platforms. Companies such as Perfios, ScoreMe, SaveRisk, Probe, Nexensus and similar platforms play an important role in this ecosystem. Their value lies in converting raw borrower information into structured signals.

A bank statement analyser, for instance, may identify transaction movement, cheque return behaviour, liquidity conduct, utilisation patterns, internal transfers, loan servicing indicators, exceptional transactions and possible stress signals. Similarly, GST, bureau, MCA and financial analytics tools can generate indicators around business scale, repayment discipline, promoter profile, leverage, related-party behaviour, compliance and governance.

This is valuable progress. But signal generation is not the same as credit judgement. The role of such platforms is to reduce raw-data burden, improve consistency, detect patterns and surface exceptions. They help the credit officer see more clearly and ask sharper questions. However, the final credit value emerges only when these signals are interpreted, bucketed, weighted and connected to a decision. Does the banking conduct support declared turnover? Does the liquidity pattern indicate comfort or stress? Are cheque returns technical, occasional or behavioural?

Are related-party transfers distorting business cash flow? Does the bureau behaviour support repayment discipline? Does the MCA profile reveal governance concerns? Does the signal require a sanction condition, monitoring trigger or risk mitigant? This is where the signal-to-judgement gap appears. If analytical outputs are merely copied into a CAM, the institution has not improved underwriting. It has only shifted from manual information gathering to digital information overload.

The tool finds the signal. The credit officer gives it meaning. Four NBFC Signals: AI Is Moving Across the Lending Lifecycle Across Indian NBFCs, the direction of travel is already visible. Relationship-led NBFCs like Sundaram Finance are exploring how technology can improve field productivity without losing customer touch. This is particularly important where lending depends on local understanding, long-term customer relationships, market knowledge and the ability to read small entrepreneurs beyond formal documents.

Cholamandalam’s discussion on Gen AI points to very practical lending use cases: document verification, legal summarisation, customer-service support, operations controls and reduced manual fatigue in verification. This is not AI for glamour. It is AI applied to real operational friction. Bajaj Finance’s FINAI ambition shows another kind of signal: AI moving from experimentation to operating strategy.

When AI is deployed across customer engagement, underwriting, productivity, controllership and cost reduction, it is no longer a side project. It becomes part of the operating architecture. Mahindra Finance’s AI direction shows that lending transformation is not limited to sourcing or underwriting. AI can enter onboarding, servicing, collections allocation, vernacular voice reminders and field-force support. That is important because lending is a lifecycle, not a sanction event.

The lesson from these NBFC signals is clear. AI must not be limited to faster origination. It must improve the entire credit lifecycle: capture, appraisal, documentation, disbursement, monitoring, servicing and collections. Four Bank Signals: Technology Exists, Judgement Conversion Is the Challenge The banking side shows a similar movement. South Indian Bank represents the journey of a traditional relationship-led bank modernising its operating model. Such banks carry deep branch relationships, customer history and regional understanding.

The challenge is not merely digitisation, but ensuring that technology supports field knowledge, credit interpretation and faster quality decisioning without weakening relationship depth. Federal Bank represents strong digital adoption. High digital transaction intensity and investments in AI and machine learning create the base for quicker decisions and personalised customer experience.

But digital intensity by itself is not the final destination. The next test is whether digital flows improve credit judgement and not merely transaction convenience. ICICI Bank represents analytics-led SME lending. Data and machine-learning decisioning across acquisition, underwriting, cross-sell, upsell and portfolio risk management show how verified data and digital public infrastructure can reduce repeated customer asks and improve decision readiness. Axis Bank represents the data-and-model-driven decisioning direction.

Machine-learning-based credit models using large numbers of attributes show how credit decisioning is moving from isolated data points to weighted, model-supported signal interpretation. Together, these examples show that banks are not short of digital infrastructure, analytics or technology ambition. The real question is different. Is the information being captured better? Is it being bucketed into credit meaning? Is it being weighted through scoring and predictive models? Is it being converted into sanction structure, mitigants, monitoring triggers and collection action? Digital maturity generates data.

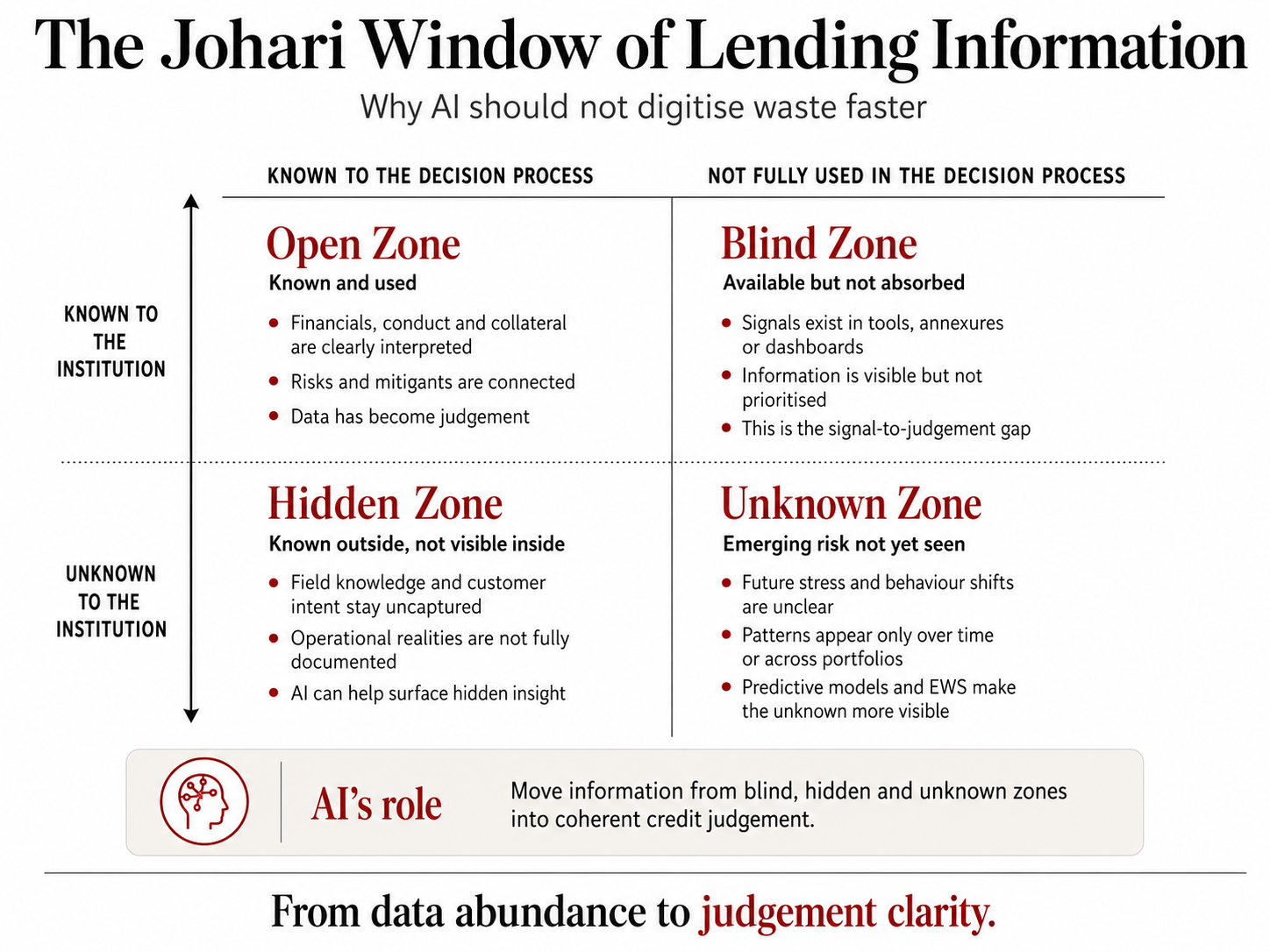

Intelligent lending converts data into judgement. The Johari Window of Lending Information The Johari Window is usually used to understand awareness in human relationships. But it also offers a powerful way to understand credit decisioning. In lending, information does not become useful merely because it exists. It becomes useful only when it is known, interpreted, weighted and applied to judgement.

The Johari Window helps us classify lending information into four zones. 1. The Open Zone: Known and Used This is information that is available to the institution and is also clearly used by the decision-maker. Audited financials, bureau behaviour, banking conduct, collateral value, repayment track record, GST trends and key ratios may all be available and properly interpreted in the CAM.

This is the ideal zone. Information is not merely captured. It is converted into credit judgement. The credit note explains what the information means, how it affects risk, what mitigants exist, and why the exposure is acceptable or not. In this zone, data has become judgement. 2. The Blind Zone: Available but Not Absorbed This is one of the most important zones in modern lending.

The information exists somewhere in the system, but it does not coherently enter decision-making. It may be present in a bank statement analyser, GST report, MCA extract, bureau annexure, dashboard, legal note, field visit report or CAM attachment. But it is not interpreted, prioritised or linked to the final credit view. This is the signal-to-judgement gap. A tool may generate 50 or 60 analytical signals.

But only a fraction may be meaningfully used in the credit decision. The rest may be annexed, pasted, ignored, repeated or left unexplained. This is not a data problem. It is a decision-design problem. The institution has information, but the decision process has not absorbed it. This is where analytical overproduction becomes a new form of waste. The problem is no longer absence of data.

The problem is abundance of unprioritised information. The 40% Signal Wastage Hypothesis In analytics-heavy credit processes, my working hypothesis is that a significant portion of generated analytical information may not be coherently converted into judgement. A reasonable estimate is that nearly 40% of generated analytical information may suffer from signal wastage.

This does not mean the information is useless. It means that the information may be generated, visible, annexed or copied, but not meaningfully interpreted or linked to the final credit decision. A signal is truly used only when it changes one of five things: It improves borrower understanding. It sharpens risk assessment. It supports a mitigant. It influences sanction structuring. It creates a monitoring or collection action. If it does none of these, it is not intelligence. It is analytical clutter.

The leakage is not from data to report. The leakage is from report to judgement. 3. The Hidden Zone: Known Outside, Not Visible Inside The hidden zone contains information that may be known to the borrower, market, field ecosystem or operating reality, but is not yet visible to the lender in structured form. Actual business stress may not be reflected in the latest financials. Informal borrowings may not be captured in bureau. Related-party routing may not be clearly disclosed. Accommodation entries may be hidden inside banking flows. Customer intent may be known to field staff but not captured in the system.

Market reputation may not be reflected in documents. Collection conversations may not be summarised for credit review. Operational weakness may not be visible in formal statements. This is where relationship-led lending still matters. Field knowledge, customer interaction, local market feedback and promoter behaviour cannot be fully replaced by formal documents. A borrower’s ability and intent may not always sit neatly inside a bureau report, GST return or bank statement. AI can help here, but only if it is designed to support human intelligence rather than replace it. It can summarise field notes.

It can detect patterns in conversations. It can compare declared business with transaction behaviour. It can highlight inconsistencies. It can prompt officers to ask sharper questions. The goal is to bring relevant hidden information into structured credit understanding. 4. The Unknown Zone: Emerging Risk Not Yet Seen The unknown zone contains risks that are not clearly known to the lender or the borrower at the time of sanction. Future sector stress. Sudden liquidity shocks. Changing customer behaviour. Early portfolio deterioration. Weak signals that are not yet obvious.

Patterns visible only across a large number of accounts. New fraud methods. Stress that emerges after disbursement. This is where predictive modelling, EWS, scoring philosophy and portfolio analytics become important. The institution’s past should teach its present underwriting. If past data shows that certain combinations of signals tend to precede default, those patterns should feed into future decisioning. If certain borrower behaviours correlate with probability of default, loss given default, roll-forward risk or recovery weakness, those signals should be weighted appropriately.

Credit judgement remains human, but it should not remain memoryless. AI can help detect emerging patterns, but governance must ensure that the output is explainable, auditable and fair. The Human Mind Needs Buckets Credit judgement is not formed by reading data mechanically. The human mind makes sense of complexity by bucketing information into meaning. A credit officer does not treat every data point equally.

Information is mentally grouped into larger judgement buckets — business strength, cash-flow quality, banking conduct, repayment discipline, promoter credibility, leverage, collateral comfort, compliance gaps, Early warning signals and overall bankability. This bucketing is necessary. Without it, the mind gets overloaded. Modern analytical tools can generate dozens of signals from bank statements, GST records, bureau reports, MCA data and transaction behaviour.

But if these signals are not organised into meaningful credit buckets, they may create analytical clutter rather than credit clarity. The analyst may paste the output into the CAM. The reviewer may see the data. The sanctioning authority may still not get the credit story. That is the signal-to-judgement gap. A signal becomes useful only when it is absorbed into a decision bucket. Does it tell us something about business routing? Does it indicate liquidity stress? Does it show repayment discipline? Does it reveal non-business credits? Does it weaken confidence in declared turnover?

Does it require a sanction condition? Does it call for monitoring action? AI should therefore not merely generate more fields. It should help organise information into decision meaning. The goal is not more data. The goal is better cognitive organisation for credit judgement. The CAM should not be a warehouse of information. It should be a map of judgement. From Bucketing to Scoring The psychology of credit judgement begins with bucketing. Scoring philosophy takes this one step further. It asks: should every bucket carry the same weight? Clearly, the answer is no.

A minor documentation gap cannot be treated the same as repeated cheque returns. A temporary seasonal dip cannot be treated the same as structural cash-flow weakness. Collateral comfort cannot fully offset poor repayment conduct. A strong promoter background may matter, but not enough to ignore deteriorating liquidity. This is where scoring models become useful. They assign weightages to input parameters based on their observed relationship with credit outcomes. Some variables may be more closely linked to probability of default. Some may influence loss given default. Some may act as early warning indicators.

Some may matter only in combination with other signals. Predictive modelling helps convert past experience into structured decision support. If past data shows that repeated non-technical bounces, falling business credits, high utilisation, weak internal cash generation and frequent ad hoc requests tend to precede stress, the model can assign higher attention to those signals. If collateral quality, documentation enforceability and recovery history affect eventual loss, they can influence LGD thinking.

The purpose of scoring is not to replace credit judgement. It is to discipline judgement. A good model helps the institution avoid two errors: treating all information equally, and overreacting to one dramatic signal while ignoring the larger pattern. Bucketing creates meaning. Scoring creates discipline. Predictive modelling creates institutional memory. A score is not a decision. It is a weighted signal placed before judgement.

The Personal Inference Line A related question is how far back a lender should look while interpreting borrower behaviour. Some institutions treat the past as permanent behavioural evidence. If there was stress eight, ten or fifteen years ago, it continues to influence the credit view. That instinct is understandable. Credit is partly about behaviour. But not all past behaviour has equal predictive value. A recent cheque return, a current liquidity issue or a repeated delay in the last twelve months cannot be treated the same as a resolved event from ten years ago.

Similarly, a one-time business setback cannot be treated the same as a repeated pattern of concealment, wilful default or governance weakness. The question is not whether the past matters. The question is how much weight the past deserves. A useful way to think about this is the Personal Inference Line. Recent, repeated and relevant behaviour should carry higher weight. Old, isolated and explained events should carry lower weight, unless they reveal continuing character risk, unresolved liability, fraud, wilful default or recurring conduct weakness.

Time period Credit treatment Weight Approach Risk perspective 0–12 months Current liquidity, repayment, utilisation, cheque returns, banking credits, GST movement, collection discipline Very high Ideal and necessary Shows present repayment ability, live stress, current liquidity discipline and immediate default risk 1–3 years Recent conduct pattern, bureau behaviour, cash-flow trend, recurring delays, account operations, repayment consistency High Ideal Helps distinguish one-off issues from behavioural pattern; useful for PD assessment and early-warning interpretation 3–5 years Business-cycle view, stability, recovery ability, seasonality, structural changes, improvement or deterioration Moderate Balanced Useful to understand resilience, business maturity and whether past stress was temporary or structural 5–8 years Historical context, old defaults, resolved stress, business setbacks, past restructuring, legacy disputes Low to moderate Cautious / case-specific Should be used as background risk context unless there is recurrence, concealment, unresolved liability or governance concern 8+ years Remote history, very old events, legacy failures, past disputes, old stress episodes Low Aggressive if overweighted Should not dominate current decisioning unless it reveals persistent character risk, fraud, wilful default, unresolved legal exposure or repeated behavioural pattern The purpose of the Personal Inference Line is not to ignore the past.

It is to give the past the right risk weight. Credit should remember the past, but not fossilise the borrower. Data analytics should help lenders distinguish history from habit, and background from behaviour. Remote History, Residual Risk and RAROC For behaviour beyond eight years, the credit question should move from eligibility to residual risk. An old adverse event should not automatically become a rejection filter. If the event is resolved and followed by sustained good conduct, it should remain background context. If some residual concern remains, the lender can reflect it through risk-adjusted structuring.

This is where RAROC becomes useful. RAROC allows the lender to ask whether the return is adequate for the residual risk being taken. Remote history may influence pricing, collateral, margin, tenor, exposure cap, covenants, monitoring frequency or early warning triggers. It need not automatically decide the proposal. In other words, old behaviour should be converted into risk-adjusted structuring, not permanent borrower condemnation. An eight-year-old event is not automatically a credit veto. It is a residual-risk question.

The CAM as the Plated Dish Credit assessment is like serving a dish to a health-conscious diner. The ingredients matter. The recipe matters. The process matters. But the final test is the dish itself — whether it is balanced, digestible, confidence-giving and fit for the person consuming it. In lending, the ingredients are data points, bank statement analytics, GST information, bureau records, financials, collateral, market feedback and conduct signals.

The recipe may be a legacy credit process, a modern digital workflow or an AI-supported model. But the final dish is the credit view. The CAM is the plated dish. A traditional recipe may still produce a good dish if it is prepared with judgement. A modern recipe may still fail if it merely assembles ingredients without balance. Similarly, a CAM filled with tool outputs, ratios and dashboards does not automatically become a strong assessment.

The question is not how much data was used. The question is whether the data was converted into a balanced, risk-conscious and bankable credit judgement. Data is the ingredient. Process is the recipe. The CAM is the plated dish. Credit judgement is the taste. Why AI Should Not Digitise Waste Faster This is where the risk becomes clear. If the process is weak, AI may simply accelerate the weakness. If there is repeated data entry, AI may help copy faster without questioning why the data is repeated. If there are 60 CAM sheets, AI may help fill them faster without questioning whether all sections add insight.

If analytics tools generate many signals, AI may generate even more summaries without helping the credit officer prioritise. If dashboards show historical numbers, AI may make the MIS more attractive without making it actionable. If collections teams lack context, AI may increase contact intensity without improving treatment quality. That is why AI should not begin as a technology question. It should begin as a Lean question: Where is the waste? And as a Johari question: Which information is known, unknown, hidden or unabsorbed? Only then can AI become meaningful.

What AI Should Actually Do AI should help move information across the Johari Window. From blind to open: by converting existing but unused signals into credit insight. From hidden to open: by capturing field knowledge, customer conversations, behavioural patterns and transaction inconsistencies. From unknown to visible: by detecting emerging patterns through predictive modelling, EWS and portfolio analytics. From clutter to judgement: by bucketing information into decision meaning.

This is the true role of AI in lending. Not to produce more information. Not to decorate the CAM. Not to replace credit judgement. But to improve the quality, timing and context in which judgement is applied. The Role of Signal Platforms Signal platforms are essential to this journey. They are not the decision-maker. They are not the sanctioning authority. They are not the credit officer. They are intelligence feeders into the credit judgement engine. Their role is to reduce manual extraction, improve data consistency, detect patterns, flag exceptions and surface signals that may otherwise remain hidden.

But lenders must avoid using them mechanically. A signal platform should not become a CAM-filling machine. It should become a judgement-support engine. Its output should help the credit officer ask sharper questions. What is the borrower’s real cash-flow behaviour? Is the banking conduct aligned with the business story? Are the inflows genuine and recurring? Are outflows explainable? Are internal transfers distorting the picture? Are stress signals emerging? Is the account behaviour consistent with the requested facility? Analytics is not underwriting. Analytics is the raw material for better underwriting.

The DMAIC Link This is where the old discipline of DMAIC remains relevant. AI does not replace DMAIC. AI makes DMAIC more intelligent. Define the lending problem. Measure the waste. Analyse the root cause. Improve the process with workflow, controls and AI. Control the outcome through dashboards, audit trails and human oversight. Without this discipline, AI risks digitising waste faster. With this discipline, AI becomes a structured improvement tool. Closing Thought The future of lending will not be won by institutions that merely generate more data, adopt more tools or launch more AI pilots.

It will be won by institutions that convert information into judgement. The Johari Window reminds us that information may be visible, hidden, blind or unknown. The human mind reminds us that information must be bucketed into meaning. Scoring reminds us that meaning must be weighted. Predictive modelling reminds us that past outcomes must improve present decisions. Signal platforms remind us that raw data can be structured into useful signals. And credit reminds us that the final test is not the quantity of information collected, but the quality of judgement produced. AI should not digitise waste faster.

It should help lenders move from data abundance to judgement clarity. That is the difference between digital lending and intelligent lending. Digital lending changes the medium. Intelligent lending changes the method. Disclaimer and Usage Notice This article is an original work of the author. Several perspectives, examples and observations reflected here have been shaped through professional engagements with people in the field, as well as informal discussions with young research students who are being mentored out of sheer passion for the subject.

The ideas have been independently structured, interpreted and articulated by the author. The views expressed are personal and intended for professional reflection and discussion. They should not be treated as institutional views, formal research findings, credit policy guidance or professional advice. No part of this article, including its concepts, structure, terminology, models, phrases or original expressions, may be copied, reproduced, adapted, republished, distributed, used in presentations, training material, commercial work or derivative content without the prior explicit permission of the author.

Limited references may be made only with proper attribution to the author and a link to the original source.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.