Episode 4: From EWS Reports to Early Warning Sensing

Why monitoring must move from periodic reporting to behavioural radar

Every stressed account has a past.

And in most cases, that past was not silent.

The account spoke.

It spoke through reduced credits.

It spoke through sticky utilisation.

It spoke through delayed stock statements.

It spoke through cheque returns.

It spoke through repeated ad hoc requests.

It spoke through stretched receivables.

It spoke through changing borrower behaviour.

It spoke through field discomfort.

It spoke through collection conversations that never reached the credit note.

The problem is not that the account did not warn us.

The problem is that the warning was scattered.

The problem is that the warning was scattered.

Credit saw one part.

Operations saw one part.

Relationship saw one part.

Collections heard one part.

The system recorded one part.

The dashboard reflected one part.

But nobody sensed the whole story early enough.

That is the weakness of traditional EWS.

It often becomes active after stress has already become visible.

It records the smoke.

Intelligent lending must sense the heat.

This is the movement required now:

From EWS reports to early warning sensing.

From periodic triggers to behavioural radar.

From “which account has breached?” to “which borrower is beginning to change?”

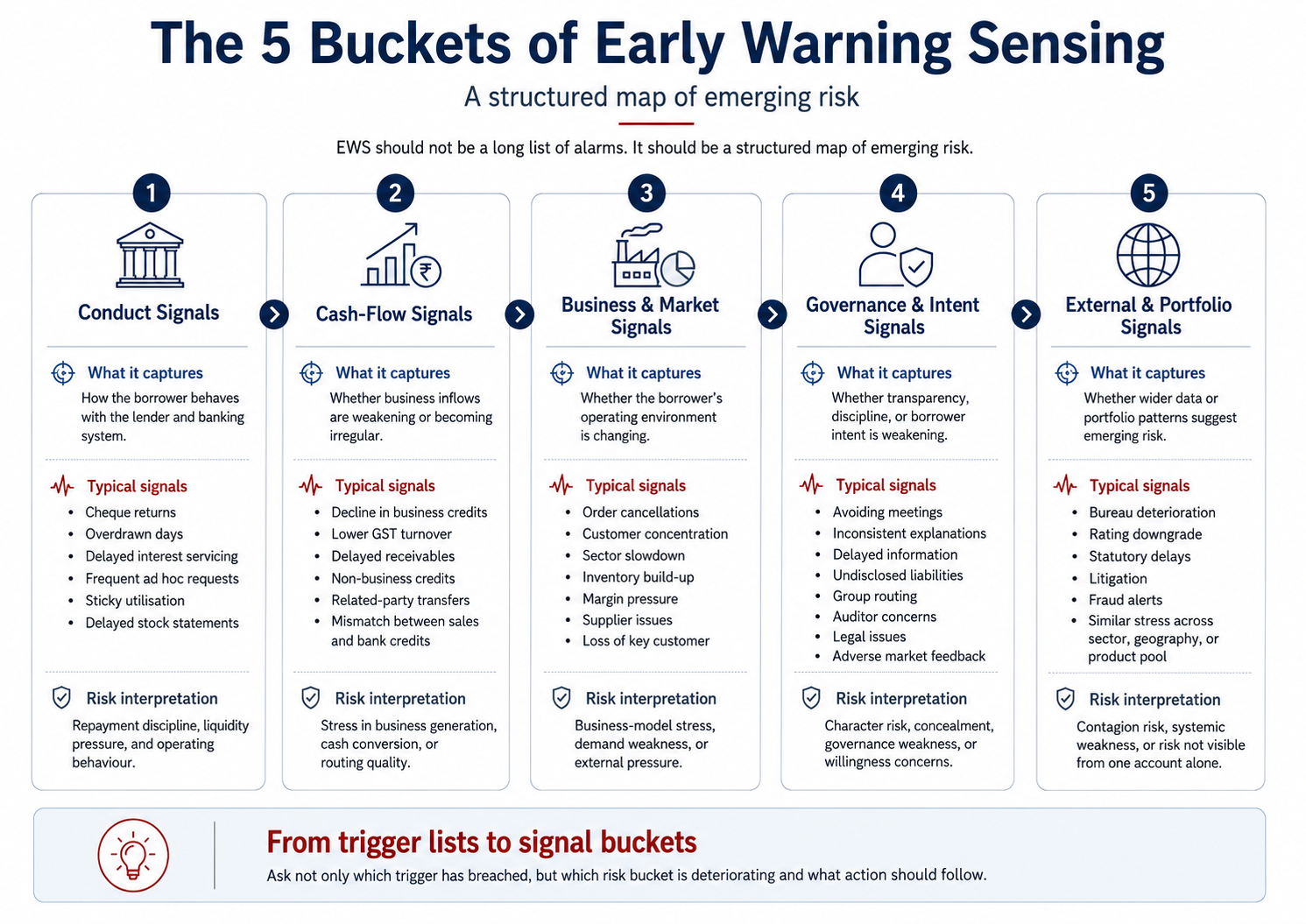

The 5 Buckets of Early Warning Sensing

For early warning to be meaningful, signals should not be seen as a long checklist. They should be grouped into decision buckets.

A credit officer does not need fifty disconnected warning points. The officer needs to know what kind of stress is forming.

Broadly, early warning signals can be grouped into five buckets:

The Difference Between an Alarm and a Radar

Traditional EWS behaves like an alarm.

It rings when a threshold is crossed.

A radar does not wait for collision. It tracks movement, direction and speed.

But lending stress is often visible before the alarm rings.

It must track whether borrower behaviour is moving away from the original credit assumption.

At sanction, the lender forms a view:

The business will generate cash.The account will route transactions.The borrower will service interest.The stock and receivables will support the working-capital cycle.The promoter will remain transparent.The risk will remain within acceptable bounds.

Monitoring is the process of testing whether that view is still valid.

If credits reduce, utilisation hardens, information delays, explanations change and commitments are missed, the account may be moving away from the original credit assumption.

That movement is the real early warning.

Not merely overdue.

Not merely SMA.

Not merely a delayed statement.

The real early warning is behavioural drift.

An alarm tells us that something has breached.

A radar tells us that something is moving in the wrong direction.

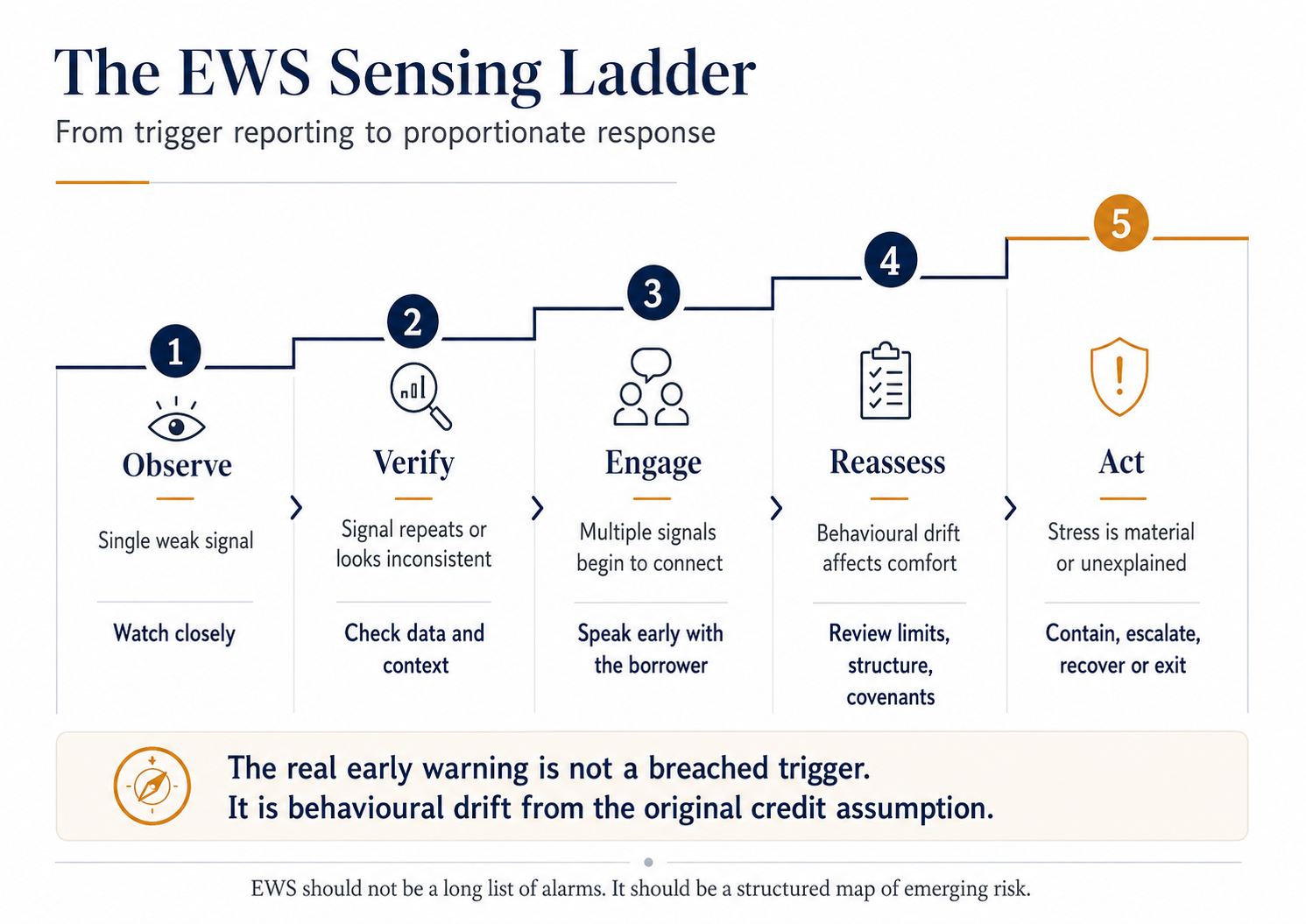

The EWS Sensing Ladder

The real value of early warning is not in identifying that a signal exists.

The value lies in knowing what level of response the signal deserves.

Not every warning signal requires escalation. Not every delay indicates stress. Not every cheque return means default. Not every fall in credits means business weakness. Not every evasive answer proves intent risk.

This is why EWS must move from trigger reporting to response design.

A useful way to think about this is the EWS Sensing Ladder.

This ladder is important because early warning should not become automated suspicion.

A good EWS system should not punish every signal.

It should help the institution decide whether the right response is observation, verification, engagement, reassessment or action.

The difference matters.

If the conduct bucket shows one delayed stock statement, observation may be enough.

If the conduct bucket and cash-flow bucket both weaken, verification is needed.

If conduct, cash-flow and governance signals start appearing together, early borrower engagement becomes essential.

If the borrower’s explanations remain inconsistent and account behaviour continues to weaken, the lender must reassess the exposure.

If the pattern becomes material, recurring or unexplained, action cannot be delayed.

This is where intelligent EWS becomes valuable.

It does not merely ask, “Which trigger has breached?”

It asks:

“What is the pattern?” “Which buckets are weakening?” “How fast is the behaviour changing?” “What is the right response level?” “Who owns the next action?” “When should the account be reviewed again?”

The purpose of EWS is not to create panic.

The purpose of EWS is to create timely, proportionate and accountable action.

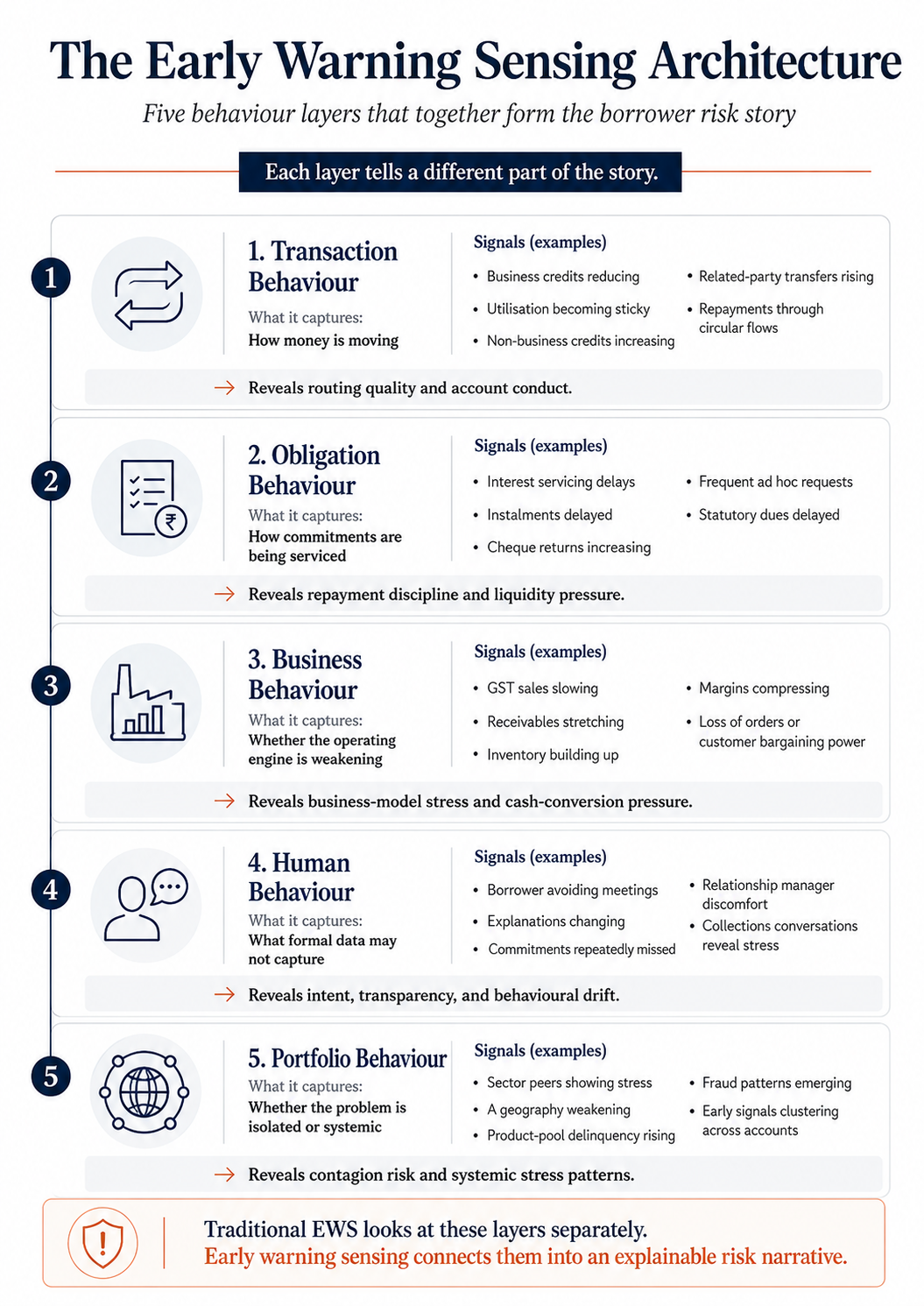

The Early Warning Sensing Architecture

To move from EWS reports to early warning sensing, lenders need more than a trigger list.

They need an architecture.

Early warning sensing must connect five layers of information:

Early warning sensing must connect them.

The account may not be overdue yet. But if transaction behaviour weakens, obligation behaviour tightens, business behaviour slows and human behaviour becomes evasive, the lender is already seeing behavioural drift.

That is the real early warning.

The value of AI is not merely in detecting each signal.

The value is in connecting the layers and presenting an explainable risk narrative.

From Data Points to Risk Narrative

A good EWS system should not merely say:

“Stock statement delayed.”

It should say:

“Stock statement has been delayed for two months, utilisation has remained high, business credits have reduced, GST turnover has softened and borrower commitments have not materialised. The account may require early engagement.”

A good EWS system should not merely say:

“Cheque return observed.”

It should say:

“Cheque returns have increased in the current quarter, interest servicing is delayed, business credits are irregular and related-party credits have increased. Liquidity discipline may be weakening.”

A good EWS system should not merely say:

“GST turnover declined.”

It should say:

“GST turnover has declined, bank credits have also fallen, receivables are ageing and the borrower has sought ad hoc support. Business cash conversion may be under pressure.”

This is the difference between a trigger and a narrative.

A trigger tells us what happened.

A risk narrative tells us why it may matter.

The future of EWS is not a longer exception report.

It is an explainable account story.

Closing Thought

EWS should not remain a post-mortem report.

It should become a behavioural radar.

The real value of AI in early warning is not to generate more alerts, longer dashboards or unexplained risk scores. Its value lies in connecting scattered signals and helping lenders see behavioural drift earlier.

AI can help identify whether conduct, cash flow, business, governance or portfolio signals are weakening. It can connect bank statement behaviour, GST trends, repayment discipline, field notes, collection remarks and portfolio patterns into an explainable risk narrative.

It can help distinguish an isolated delay from a recurring pattern.

It can help separate noise from emerging stress.

It can help prioritise which account needs observation, verification, engagement, reassessment or action.

But AI should not replace human judgement.

It should improve the timing, quality and context in which judgement is applied.

Because monitoring is not a post-sanction formality.

Monitoring is the continuation of underwriting.

At sanction, the lender forms a view of the borrower. Early warning sensing tests whether that view is still valid.

Digital lending tells us what happened.

Intelligent lending helps us sense what is changing.

Disclaimer and Usage Notice

This article is an original work of the author and is intended for professional reflection and discussion. The perspectives expressed here are personal and should not be treated as institutional views, formal credit policy, regulatory guidance, or professional advice.

Some observations and examples in this article are shaped by professional experience, discussions with people in the field, and informal mentoring conversations with young research students pursued out of passion for the subject. The concepts, structure, interpretation and articulation are independently developed by the author.

No part of this article, including its concepts, frameworks, terminology, models, diagrams, phrases or original expressions, may be copied, reproduced, adapted, republished, distributed, used in presentations, training material, commercial work or derivative content without the prior explicit permission of the author.

Limited references may be made only with proper attribution to the author and a link to the original source.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.