A colleague asked whether AI adoption in banks really has depth. I paused to examine the public evidence.

A colleague who had been reading my recent blogs on AI in lending called me with a simple question:

“Is there really so much depth in AI adoption within banks, or are we overstating it?”

It was a fair question.

Most of us hear the words AI, GenAI, machine learning, analytics and automation almost every day now. They appear in conferences, vendor presentations, LinkedIn posts, annual reports and leadership conversations. But beyond the language, what is actually visible? Are banks merely experimenting with chatbots and digital journeys? Or has AI begun entering the real operating layers of banking — credit, fraud, underwriting, monitoring, collections, compliance and employee productivity?

This blog is an attempt to answer that question.

Not through opinion.

Not through hype.

But by pausing and looking at what banks themselves are publicly disclosing through annual reports, investor presentations, official filings and leadership commentary.

The purpose is not to rank banks or declare winners and laggards. Different banks disclose differently. Some may be doing meaningful work internally without describing it in detail publicly. Therefore, absence of disclosure should not be read as absence of adoption.

Let us look at the evidence through a few statistical cuts. :

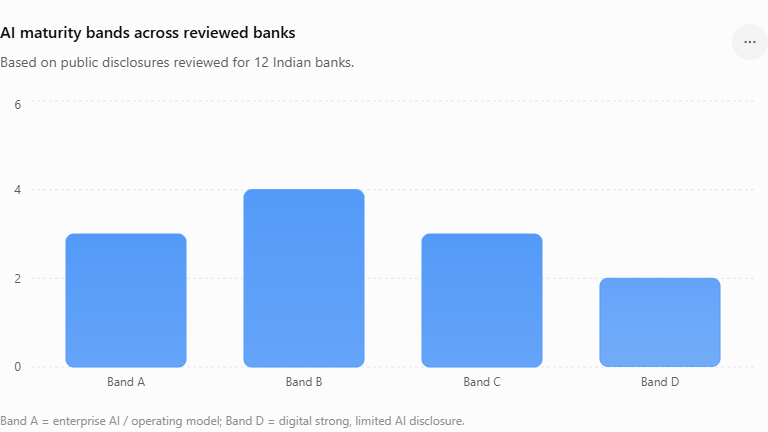

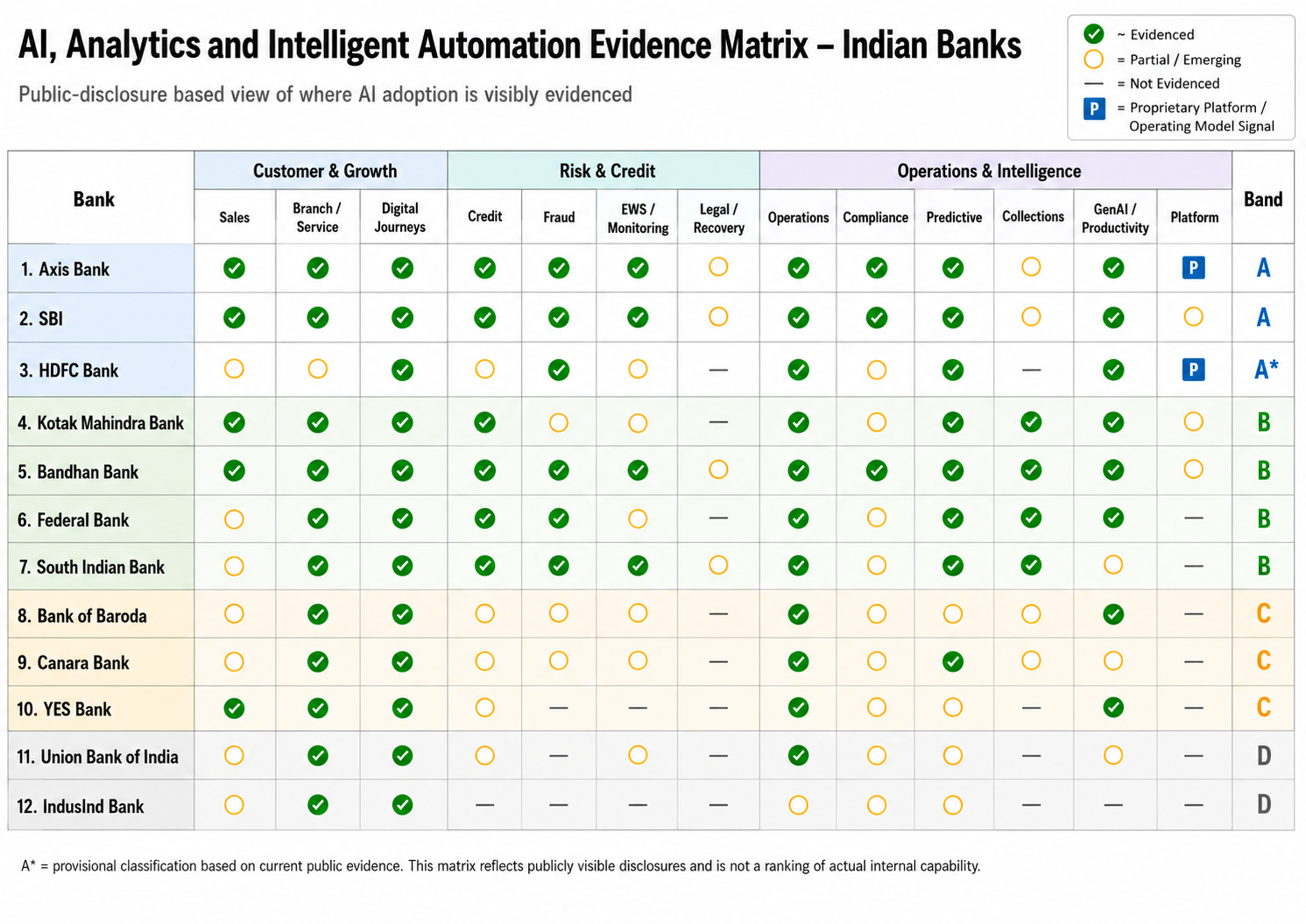

To make sense of the evidence, I have grouped the banks into four maturity bands.

This is not a ranking of capability.

It is only a public-disclosure based view of where AI, ML, GenAI, analytics or intelligent automation appear to have entered the banking operating model.

The bands move from enterprise AI adoption at one end to digital transformation with limited AI disclosure at the other.

Four maturity bands

Band A — Enterprise AI / operating model

AI is visible as a platform, operating model or enterprise-scale capability.

Band B — AI embedded in credit, risk and collections

AI / analytics is visible in underwriting, fraud, EWS, monitoring, collections or recovery.

Band C — AI-enabled service and operations

AI is visible mainly in customer service, branch support, RPA, digital journeys and process automation.

Band D — Digital strong, AI disclosure limited

Digital transformation is visible, but public AI-specific disclosure is still limited.

Visual 1 — Maturity band distribution

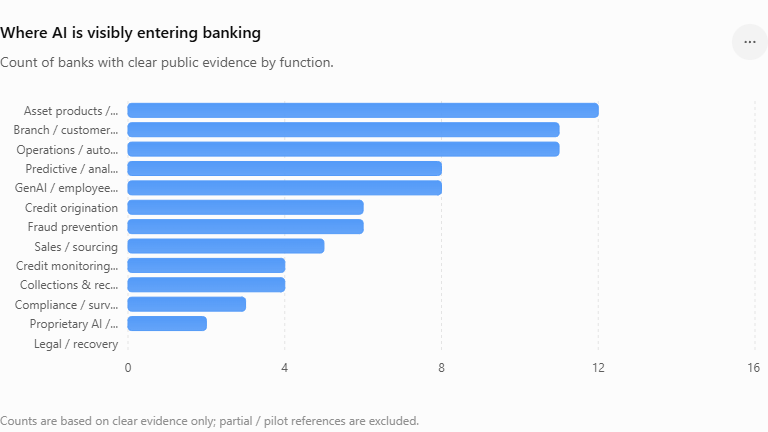

Visual 2 — Function-wise AI evidence

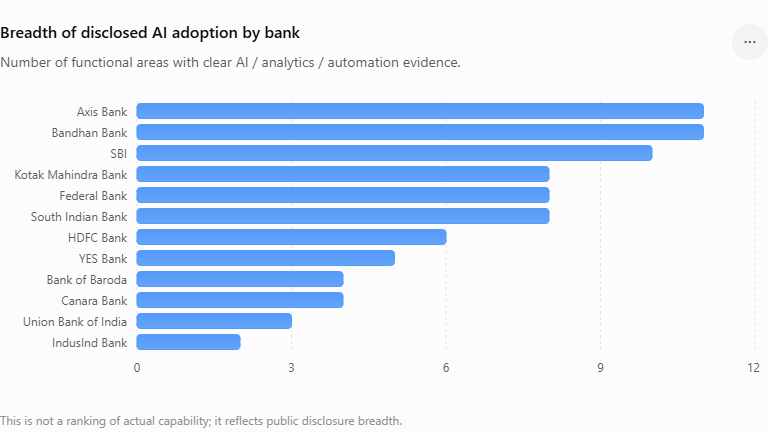

Visual 3 — Adoption breadth by bank

Core evidence matrix

What the numbers suggest

The adoption story is real — but uneven.

AI is most visible in customer service, digital journeys, operations and analytics. That is expected. These are lower-friction areas for adoption.

The more interesting evidence is in credit, fraud, EWS and collections.

Several banks now disclose AI-assisted credit decisioning, ML scorecards, predictive collections, fraud monitoring, early warning signals, risk analytics and GenAI-based employee tools.

That means AI is beginning to move beyond the front-end interface.

It is entering the operating system of banking.

Closing thought

The question is no longer:

“Are banks using AI?”

The better question is:

“Where has AI entered the banking operating model?”

The public evidence suggests that AI in Indian banking is moving from experimentation to infrastructure.

But the maturity gap is visible.

Some banks are building AI operating models. Some are embedding AI into credit, risk and collections. Some are still using AI mainly for service and operations. Some disclose strong digital transformation, but limited AI depth.

That is the real map.

AI adoption in banking is not hype.

But neither is it uniform.

The next differentiator will not be the presence of AI.

It will be the responsible embedding of AI into credit flow, fraud monitoring, early warning sensing, decision cockpits, collections, compliance and human-supervised judgement.

Disclaimer

This article is based on a review of publicly available information, including annual reports, investor presentations, official filings, bank disclosures, media reports and leadership commentary available at the time of writing.

The purpose of this article is not to rank banks, certify AI capability, or comment on the actual internal technology maturity of any institution. It is only an evidence-based attempt to understand where AI, ML, GenAI, analytics and intelligent automation are visibly disclosed across the banking operating model.

Absence of public disclosure should not be interpreted as absence of adoption. Similarly, presence of disclosure should not be read as an assessment of effectiveness, governance quality, model performance or implementation depth.

The views expressed are personal and intended for professional discussion. Many of the themes have also emerged through informal engagements with practitioners, colleagues, field professionals and young research students whom I mentor out of interest in the subject.

The content, structure, interpretation, maturity bands and framework used in this article are original to the author. No part of this article may be copied, reproduced, adapted, republished or used without the explicit permission of the author. Limited references are permitted only with proper attribution to the author and link to the original source.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.