Episode 2: The AI Lending Flywheel From Isolated Use Cases to Intelligent Credit Flow In Episode 1, we looked at the hidden waste in lending. Paper is visible. But the deeper waste lies elsewhere — waiting, repeated data entry, duplicate documentation, manual verification, delayed clarifications, compliance rework, dashboard noise and experienced human judgement being spent on low-value checking.

The natural next question is: what should transformation do about this? The answer is not to add AI randomly into every process. The answer is to build an intelligent credit flow. This is where the idea of the AI Lending Flywheel becomes useful. Why a Flywheel? A lending institution is not merely approving loans. It is repeatedly performing a cycle: It sources customers. It captures information. It understands the borrower. It assesses risk. It documents conditions. It disburses. It monitors. It collects. It learns from outcomes.

In many institutions, these stages operate like separate compartments. Sales captures information. Credit assesses. Operations checks. Legal reviews. Compliance validates. Collections follows up. Risk monitors. Management reviews dashboards. Each team works hard. But the process often does not learn as one system. The same information is captured again. The same document is checked again.

The same risk is explained again. The same exception is discovered late. The same customer is contacted without full context. The same portfolio signal appears only after stress is visible. This is not intelligent flow. It is fragmented flow. A flywheel changes the logic. In a flywheel, every rotation adds momentum. Every stage improves the next stage. Every outcome feeds back into future decisions. That is what AI should help create in lending.

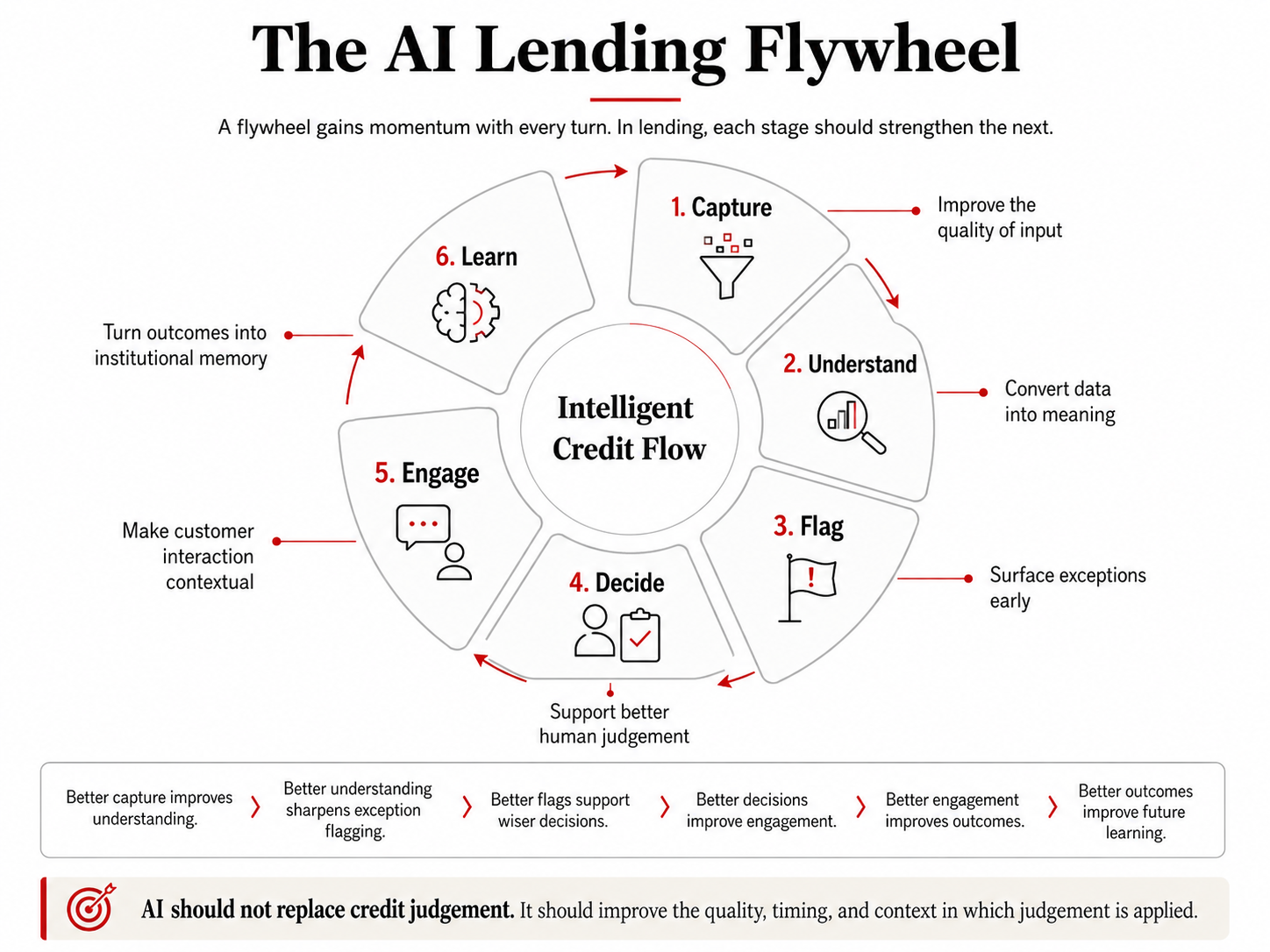

The AI Lending Flywheel The AI Lending Flywheel has six stages: Capture --> Understand ---> Flag --->Decide ---> . Engage ---> Learn. This model is deliberately simple. It is not meant to replace lending judgement. It is meant to show where technology can support judgement. The objective is not to remove people from lending. The objective is to remove friction around people so that their judgement is used where it matters most. 1. Capture: Improve the Quality of Input The first stage is capture. Most lending errors begin much before the credit decision. They begin at the point of information capture.

DATA CAPTURE ISSUES Customer details are entered incorrectly. Documents are uploaded without proper tagging. Financial data is keyed in manually. Field remarks are typed briefly or inconsistently. Regional language inputs are lost or poorly translated. Customer conversations are not structured for future use. When input quality is weak, every later stage suffers. Credit asks for clarification. Operations finds mismatch. Legal asks for more documents. Compliance finds gaps. Collections lacks context. Dashboards become unreliable. AI can help improve capture. It can read documents. It can extract fields.

It can classify uploads. It can convert voice inputs into text. It can support regional language capture. It can prompt frontline teams to collect missing information at the source. 2. Understand: Convert Data into Meaning The second stage is understand. Lending institutions already collect a lot of information. But information is not the same as understanding. A bank statement is information. Understanding cash-flow behaviour is judgement. A GST return is information. Understanding business momentum is judgement. A bureau report is information. Understanding repayment intent is judgement.

A customer visit note is information. Understanding the promoter’s credibility is judgement. A CAM is not merely a container of information. It should be evidence that the borrower has been understood. AI can support this stage by summarising, comparing, organising and connecting information. It can summarise business documents. It can identify key financial movements. It can compare bank credits with declared turnover. It can identify repeated patterns in conduct. It can summarise legal documents. It can consolidate field inputs. It can help identify whether the credit story is consistent across sections.

But AI should not be confused with judgement. Understanding in lending requires context. The role of AI is to prepare the ground better so that human judgement can operate with more clarity. 3. Flag: Move from Manual Search to Exception-Led Review The third stage is flag. This is one of the most important shifts in lending transformation. In many lending processes, people manually search for errors, gaps and mismatches. They check whether documents match system entries. They check whether financial numbers match annexures. They check whether policy deviations are listed.

They check whether approval conditions are captured. They check whether collateral details are consistent. They check whether legal and valuation reports are aligned. Some checking is necessary. But when experienced people spend excessive time searching for routine mismatches, judgement is wasted. AI can help move the institution from manual checking to exception-led review. Let the system compare routine fields. Let the system identify missing information. Let the system highlight inconsistencies. Let the system flag overdue conditions. Let the system detect repeated deviations.

Let the system show what needs human attention. Then let experienced people review the exceptions. This protects human judgement. It also improves control quality. A tired checker may miss a problem. An exception-led system can help ensure that attention is focused where risk is higher. The objective is not to remove the human. The objective is to remove fatigue from the human role. 4. Decide: Keep Judgement Human, But Better Supported The fourth stage is decide. Credit decisions must remain judgement-led. AI should not become a black box that decides who deserves credit.

Lending is too contextual, too regulated and too relationship-sensitive for that. But AI can improve the quality of decision preparation. It can show what has changed. It can summarise key risks. It can compare borrower behaviour over time. It can highlight policy exceptions. It can identify missing mitigants. It can detect whether the recommendation flows logically from the facts. It can show whether similar past cases behaved well or badly.

This is where AI can be most useful to credit committees and sanctioning authorities. Not by replacing the decision-maker. But by improving the decision environment. A good credit decision requires facts, interpretation and accountability. AI can help organise facts. It can support interpretation. It can improve consistency. It can create a better audit trail.

But accountability must remain human. The future of lending is not black-box approval. It is better-supported human judgement. 5. Engage: Make Customer Interaction More Contextual The fifth stage is engage. This is especially important for relationship-led NBFCs and lenders serving small entrepreneurs, vehicle owners, traders and self-employed customers. In such businesses, lending is not only a digital transaction. It is a relationship built through field contact, local knowledge, repayment history, conduct and trust. Technology should not weaken this human touch. It should strengthen it.

AI can help frontline teams engage better. It can summarise the customer’s history. It can show prior commitments. It can highlight unresolved issues. It can prompt the officer with relevant information. It can help explain why a document or condition is required. It can support communication in regional languages. It can help collections teams understand repayment behaviour before contacting the borrower.

This matters because not every customer issue is the same. A genuine cash-flow mismatch is different from habitual delay. A documentation gap is different from avoidance. A confused customer is different from a wilful defaulter. A seasonal delay is different from structural stress. AI can help teams engage with better context. The goal is not to make lending impersonal.

The goal is to make relationship-led lending more informed. 6. Learn: Convert Outcomes into Institutional Memory The sixth stage is learn. This is where the flywheel becomes powerful. Most institutions have rich experience, but not all experience becomes institutional learning. A proposal was approved. What happened later? A deviation was accepted. Did the risk materialise? A collateral comfort was relied upon. Did it help? An EWS signal was ignored. Did the account deteriorate? A CAM weakness was corrected. Did similar errors recur? A collection promise was broken. Was it visible earlier? A segment grew fast.

Did stress follow? AI can help convert outcomes into learning. It can analyse which exceptions later became stress. It can identify recurring CAM errors. It can show which branches repeatedly miss documentation. It can detect which policy deviations need tighter control. It can identify which early-warning signals are most predictive. It can help refine collections strategies based on borrower behaviour.

This is the final stage of intelligent lending. The system should not merely process loans. It should learn from what happened after processing them. Why This Is Different from AI Use Cases Many AI discussions begin with use cases. Document extraction. Chatbots. Credit scoring. Legal summarisation. Customer service prompts. Collections prioritisation. Dashboard automation. These are useful.

But they can remain fragmented if they are not connected to a larger operating model. The flywheel gives the operating model. It asks: What are we capturing? What are we understanding? What are we flagging? What are humans deciding? How are we engaging? What are we learning? This keeps AI grounded in the lending journey. It also prevents AI from becoming a fashionable experiment. flow of credit judgement?

The question is not: where can we use AI? The question is: where can AI improve the flow of credit judgement ? The CAM and the Flywheel The Credit Assessment Memo is a good example. In many institutions, the CAM becomes a large document containing repeated information across multiple sections. Business profile. Financials. Banking conduct. Collateral. Deviations. Risks. Mitigants. Recommendation.

The same fact may appear in different forms in different places. If inconsistently presented, it weakens confidence in underwriting quality. A weakly worded CAM does not automatically mean weak assessment. But it creates doubt about whether the assessment was complete, connected and consciously reasoned. In the AI Lending Flywheel, the CAM should not be a dumping ground for information. It should be the output of intelligent flow. Capture should ensure the data is correct. Understand should connect facts into meaning. Flag should identify gaps and inconsistencies. Decide should preserve human credit judgement.

Engage should ensure customer and field context is reflected. Learn should identify whether past assumptions were right. This is how CAM quality improves. Not by asking analysts to fill more sheets. But by improving the system through which credit judgement is captured and communicated. From Dashboards to Decision Cockpits The flywheel also changes how dashboards are viewed. Traditional dashboards show what happened. Logins. Disbursements. Turnaround time. Overdue. SMA. NPA. Collection efficiency. Pending files. These are useful, but incomplete. An AI-enabled decision cockpit should show what needs attention.

Which accounts have changed behaviour? Which files are stuck and why? Which branches have repeated documentation gaps? Which deviations are recurring? Which borrowers show early stress despite being regular? Which customers need support, discipline or escalation? Which portfolio signals need management attention? MIS is a mirror. Most MIS in lending suffers from what may be called the Darpan Effect. A darpan, or mirror, shows what is already visible. It reflects the present or the past. It does not warn. It does not prioritise. It does not interpret. It does not tell the viewer where to act.

A decision cockpit must become a radar. That is the shift from reporting to sensing, from visibility to prioritisation, and from dashboarding to decision support. The Darpan Effect is when dashboards reflect the past but fail to direct attention to the future. Governance: The Flywheel Must Be Auditable In regulated lending, AI cannot be mysterious. Every AI-supported flag, summary or recommendation must be explainable and auditable.

The institution must know: What data was used? What data was excluded? What was flagged? Why was it flagged? Who reviewed it? Who overrode it? What was the basis? What was the final outcome? Without this, AI can become operational risk. The AI Lending Flywheel must therefore be built on governance. Explainability. Audit trails. Human oversight. Data controls. Fairness. Role clarity. Outcome measurement.

The objective is not only speed. The objective is better lending quality. Leadership Implication For leaders, the flywheel creates a practical way to think about AI. Do not begin with technology. Begin with the lending journey. At each stage, ask: What information is being captured? Is it usable? Is it being understood? Are exceptions being flagged early? Are humans deciding with the right context? Are customer interactions informed? Are outcomes feeding back into future decisions? If the answer is no, that is where transformation is required. AI should not be used to decorate the process.

AI should be used to improve the flow of judgement. Closing Thought The first stage of transformation made lending digital. The next stage must make lending intelligent. That will not happen through isolated AI pilots. It will happen when lending institutions combine AI with the disciplines we have long understood — Kaizen, Lean Six Sigma and DMAIC. Kaizen reminds us that transformation is not always a dramatic event. It is often the continuous removal of small frictions: one repeated entry, one avoidable clarification, one delayed exception, one unnecessary check, one dashboard that does not lead to action.

Lean Six Sigma reminds us to remove waste, reduce defects and control variation. DMAIC gives the method: Define the lending problem. Measure the waste. Analyse the root cause. Improve the process with the right mix of workflow, controls and AI. Control the outcome through dashboards, audit trails and human oversight. The AI Lending Flywheel then becomes the operating model: Capture Better → Understand Deeper → Flag Earlier → Decide Wiser → Engage Smarter → Learn Continuously AI should not replace credit judgement. It should improve the quality, timing and context in which judgement is applied.

That is how lending moves from paperless processing to intelligent credit flow — not by abandoning old process disciplines, but by renewing them with intelligence. Copyright and Usage Disclaimer This article, including the concepts, structure, terminology, models and original expressions used herein, is the original work of the author. No part of this content may be copied, reproduced, republished, adapted, distributed, quoted extensively, used for training material, presentations, commercial purposes or derivative works without the prior written permission of the author.

Brief references may be made with proper attribution to the author and a link to the original article. Any unauthorised use, reproduction or modification of this content is strictly prohibited.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.