It was one of our chai sessions, when discussions meandered into questioning the need for a separate underwriting faction. The hypothesis :

“Credit Assessment / Underwriting as a process is a drain / bane, in the RURAL FINANCE background. “

Instead of straightaway being judgemental, I stepped back to quietly recalling

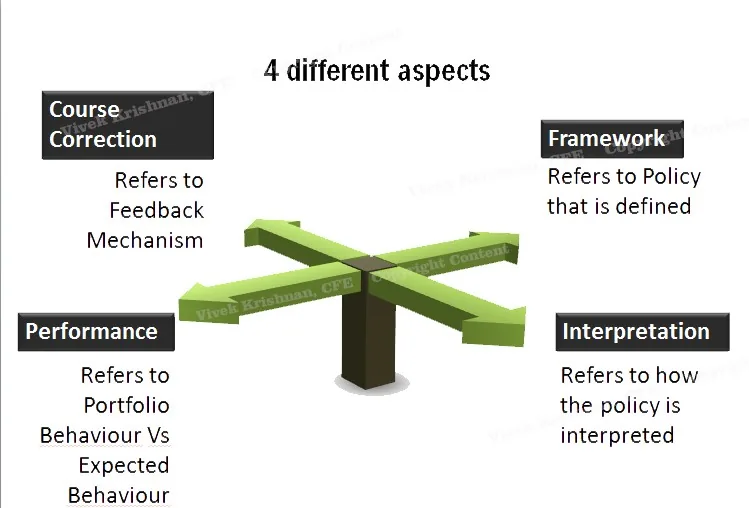

(a) Key Assumptions / Preparatory to Credit Assessments

(b) Objective of conducting credit assessments

Both these seen from a Risk Officer’s view, which would encompass Sales, Credit, Operations, Marketing, Collections, Risk / Policy Governance, and Risk Containment (Frauds / Vigilance etc.)

Why Underwriting ? Do we need it ?

The start point is a theory that different factions of business, function at different altitudes. Hence the perception of the BIG PICTURE of Policy Framework is different from different factions.

Many a time- herding, chinese whispers, interpretational issues etc., take many of us away from reality, and many a time, we keep seeing different BIG PICTURES.

In the original design, the Underwriting function, was expected to anchor these multiple BIG Pictures into one seamless process structure that each of the factions could plug into.

So how is the framework arrived at ?

The uniqueness about the framework is that it is customized. This is linked with the strategy and risk appetite of the company, clubbed with multiple other features at various levels.

The framework seeks to segment the SUBJECTIVE and OBJECTIVE part of the company’s policy. Some key points that we may note here :

(a) Both the subjective and objective parts have interpretational biases attached. Let’s take an example to understand this.

a. OBJECTIVE INTERPRETATIONAL BIAS : Let us say we define, FOIR (Fixed Obligation to Income Ratio) as 30%.

i. Bias 1 : FOIR calculated with Annualized Obligation Vs Total Obligation

ii. Bias 2 : Obligations that will count for FOIR. Jewel Loan / Credit Card Exclusion.

iii. Bias 3 : Secured Obligation Vs Unsecured Obligation

The Combination can go on…. While the policy would have felt that the FOIR definition in policy is objective, interpretations at multiple levels can create confusions.

b. SUBJECTIVE INTERPRETATIONAL BIAS : Marginal profiles, let us say, is defined as a Agri Profile with less than 4 Acres of land holding.

i. Bias 1 : Agri Land Holding of the Borrower only is considered to Qualify

ii. Bias 2 : A Farmer who leases land with no land of his own is seen to Qualify

iii. Bias 3 : Father Holding 6 Acres, with 2 Sons and one son who is borrower is seen to qualify.

Many a time, we attempt to reduce subjectivity by partially metricizing them. Yet, when the benefits are good, newer interpretations will be born by the minute to force fit actuals to pre-set definition, to avail the benefits.

The remarkable part of these biases is that you cannot deny the hypothesis presented and the interpretation. Technically, they would qualify. However, the larger aspect – Is that the intent of the policy. Is the framework mandate / definition consistent with the interpretation ?

(b) The framework needs to be unique, and yet to the customer, should seem seamless and comparable to other choices that he / she has. A very niche policy structure would require a well equipped marketing team to capitalize.

So what is the Underwriting team expected to do ?

Assess & Evaluate Proposals in an unbiased manner with the intent of accepting the proposal.

- Understand and Bridge Interpretational Fallacies

- Fit – Correct Product Offering to the Apt Profile

- Interpret – Policy and its requirement and take an unbiased call on the conservative side.

- Communicate – Get information from the market, and align to the interests of the organization

- Measure – Assess if the judgement / call taken was right, on “post facto” basis.

- Corrective Action – Ensure tweaks are effected to Policy to align with the requirements.

- Patterning & Bucketing – Create Profile Types, Assess their homogeneity, align with geographic locations, and market conditions, to aid the policy create special offerings.

- Disseminate – Walk across to various factions / users of policy to train them on the needs of the policy and organization

- Weeding – To kill / Prevent / restrict, entry of profiles, through incorrect / incomplete information, with malafide / questionable intent.

Many of us feel the pain with the Credit Function, because the act of Assessment or Weeding, is clubbed with pre-conceived notions / assumptions, and are not fact based assessments.

The Act of Underwriting demands that we “Empty the Cup” after every case.

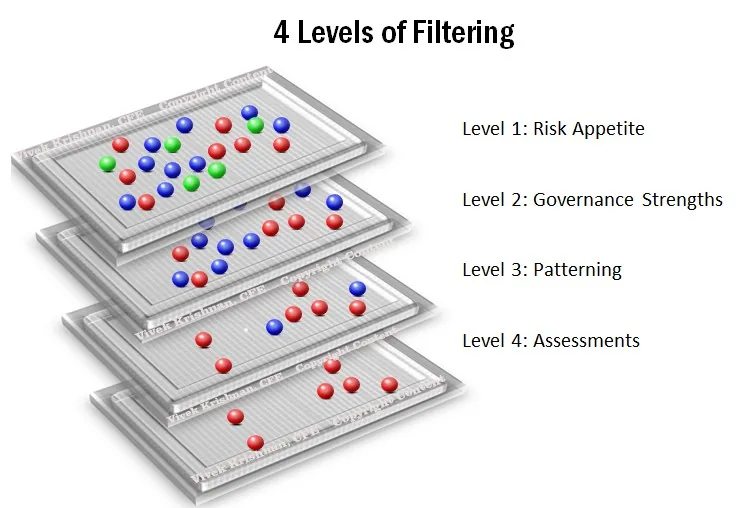

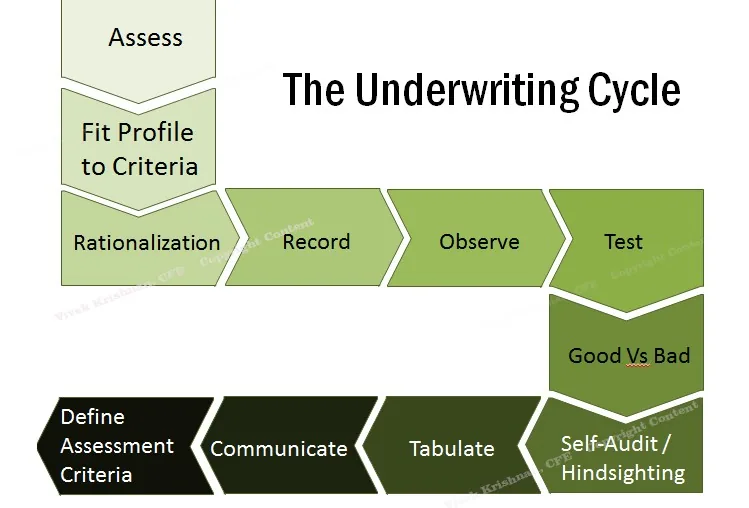

From an Underwriter’s safe guard perspective… we can broadly tabulate the process as shown in the figure below.

So, the function of Underwriting ensures :

- That the “blind spots” of stake-holders are addressed

- Serves as a platform of “Alignment” – Policy Interpretation and Implementation Governance

- Serves as “Checker” – validation mechanism in the MAKER-CHECKER Concept

- Serves as a Guardian – Integrates Policy to its implementation and serves as guardian serving multiple interests

- Serves as a Validation Point – Connects pieces of information to see if facts are consistent with profile.

Having said these, Underwriting bereft of Market Realities and Checks is only 40% efficient. A good underwriter, like his other departmental counter-parts has to be in-touch with the market. The prime difference between human underwriting to an algorithmic approach is this intelligence, which is constantly changing, based on changing market environments. We call this “Domain Intelligence”.

Given this backdrop, we need to evaluate if our Underwriting Practices, are aligned to this requirement. It does not matter if Underwriting is done Centralized / De-Centralized, the philosophy is the same. Many a time, we find the activity of Underwriting broadly under-mined and misunderstood.

Underwriting is integral and key to recording the portfolio performance. It is NOT done with a view to reduce NPAs, or reduce Collections efforts or weed out frauds. They are book-keepers merely defining the way entries are made, and ensure that the Policies designed are effective, and aid in keeping the portfolios of the company healthy.

Archive note

This essay was restored from Vivek Krishnan’s LinkedIn archive. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.