BEYOND RATIOS SERIES

Introduction

Imagine Suresh, who runs a small engineering job works unit in Rajkot, Gujarat. He fabricates precision parts for local textile machinery manufacturers. Most of his payments come via NEFT or UPI from three mid-sized clients. His account reflects ₹2.2 lakh in monthly credits — all verifiable, digital, and consistent.

Yet when he applied for a working capital facility, the branch manager flipped through his file and said, “Where’s your last three years’ audited balance sheet and collateral documents?”

Suresh, perplexed, opened his bank app: “Aren’t these monthly credits proof enough of my business activity?”

This mismatch — between authentic digital trails and legacy credit comfort zones — is exactly what the Account Aggregator (AA) framework was meant to bridge. But even in 2025, it remains underutilized in mainstream MSME underwriting.

1. AA: A Brilliant Blueprint, Yet to Scale

The RBI’s Account Aggregator framework was designed to give borrowers control over their financial data and enable lenders to make data-backed credit decisions, especially for thin-file MSMEs.

But the results so far are mixed:

Hit rate of ~40% data fetch success in early use cases

Patchy participation from major private banks (Axis, Federal, CSB, KVB, etc.)

Underwhelming adoption in MSME credit pipelines

In principle, AA should allow:

✅ Real-time account data fetch✅ Income pattern recognition

✅ Consent-based, secure sharing

But in practice, lenders are still stuck in a comfort zone of paperwork.

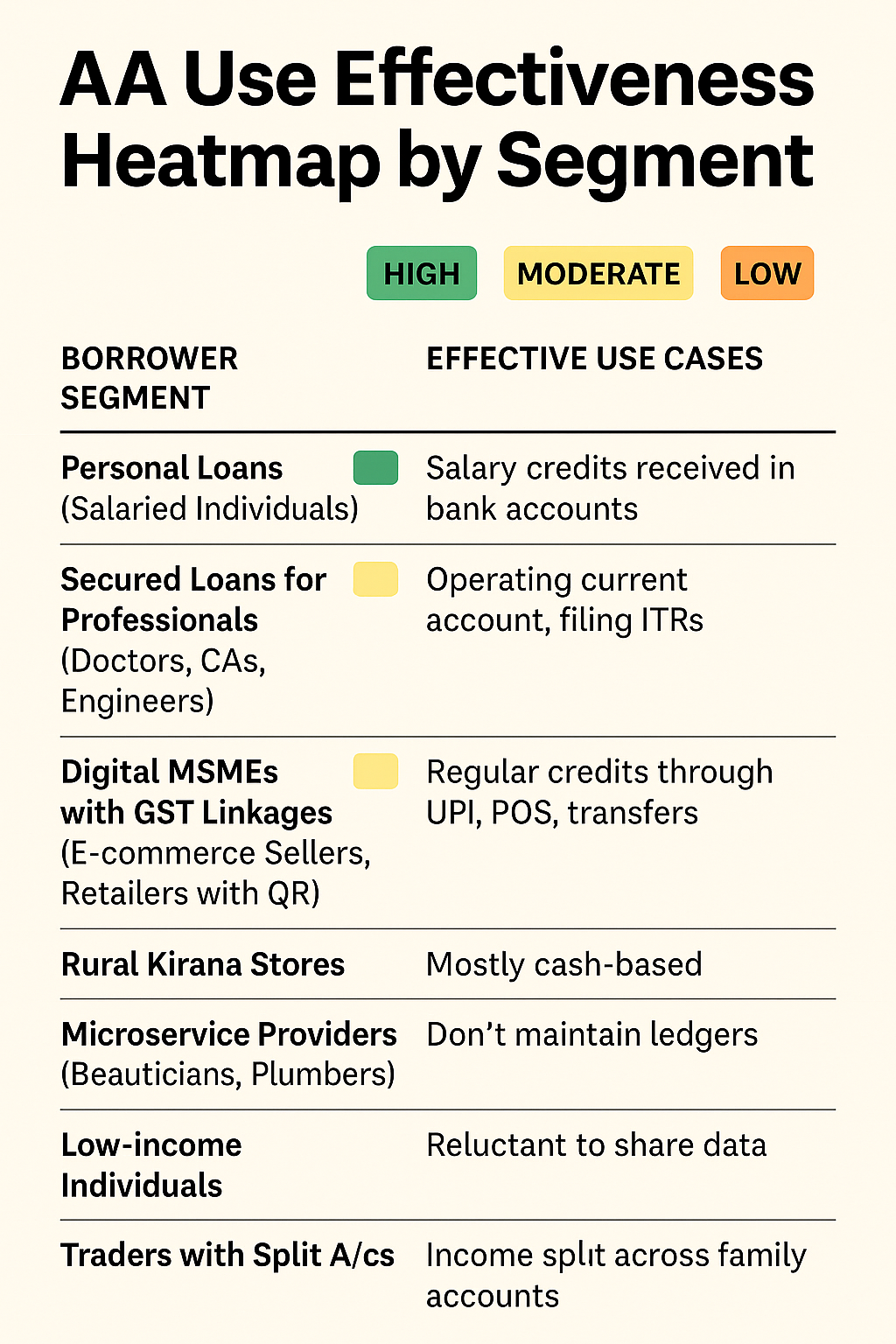

2. Who Is Using AA Effectively?

Fintechs and NBFCs targeting salaried gig workers and urban micro-enterprises are leading the charge:

Segment | Adoption Level | Use Case |

Digital lending NBFCs | High | Bureau + AA-driven underwriting |

Neo-banks | Medium | Alternate scoring for retail/gig credit |

PSU Banks | Growing | Pilots in ECLGS, personal loans |

Private Banks | Low to Patchy | Limited MSME penetration |

A heatmap visualization clearly shows that effective usage remains confined to niche lenders — while the vast MSME segment remains underserved.

3. Why Are Mainstream Banks Still Holding Back?

Despite being ‘live’ on Sahamati’s registry, many banks do not actively process AA data. Some reasons:

Legacy Core Systems: Not AA-ready for seamless data fetch

Risk Aversion: Preference for audited/verified static documents

Customer Reluctance: Users unwilling to give digital consent or unaware

Limited Internal Usage: Credit teams not yet trained to interpret AA insights

Bank | AA FIP Status | MSME Use Case Deployment | Reason for Limited Usage |

Axis Bank | Live | Partial | Legacy core systems integration gaps, inconsistent AA returns |

Federal Bank | Live | Minimal | Consent UX friction, limited MSME-focused use cases |

Karur Vysya Bank | Live | Very Low | Small FIU coverage, low AA API readiness |

CSB Bank | Live | Very Low | Rural/SME coverage gaps, low digital onboarding |

City Union Bank | Live | Limited | Focused on traditional lending verticals |

DBS Bank | Live | Limited | AA used primarily for retail/personal, not MSME |

RBL Bank | Live | Low | Lack of deeper MSME integration via AA |

Yes Bank | Live | Partial | Operational in retail, but minimal AA-driven MSME lending |

4. Bridging Policy Intent with Ground Reality

The policy vision is crystal clear: use AA to democratize credit. But ground-level friction remains high.

“Bridge policy intent with grassroots realities” means translating lofty digital reforms into tools that actually work for Suresh the engineering job works entrepreneur, or Priya the gym trainer.

Seasonality, for example, is a huge factor. A fabrication unit earns peak income during production surges for textile clients but dips when orders are low. AA-based data can show these cycles — but only if banks look beyond point-in-time balances.

5. The Way Forward

Stakeholder | Actionable Step |

Banks | Move from registry participation to use-case integration |

MSMEs | Awareness of AA and digital consent mechanisms |

Fintechs | Build AA-first scoring overlays, especially for cash-flow based models |

Policymakers | Incentivize meaningful usage over mere compliance |

Conclusion

India’s credit revolution cannot succeed without unlocking the power of real-time financial behavior. Account Aggregators were meant to be that key. But unless more banks, especially private ones, actively participate — we risk losing momentum.

Let’s not turn a promising reform into a missed opportunity.

Disclaimer:

The views expressed in this article are personal and intended for informational and thought-leadership purposes only. They do not represent the official position of any institution or employer. The examples used — including characters like “Suresh” — are fictional composites drawn from real-world scenarios for illustrative clarity. This article does not constitute financial advice, nor does it endorse any specific product, platform, or regulatory outcome. Readers are advised to consult appropriate professionals and verify facts independently before drawing conclusions or making lending decisions.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.