BEYOND RATIOS SERIES - EPISODE 3

Introduction

Ramesh runs a flourishing tailoring unit in Tirunelveli. His clients are mostly regulars from his WhatsApp group and neighbourhood references. His inflows come through UPI, small cash deposits, and advance payments via PhonePe. But when asked for a CMA (Credit Monitoring Arrangement) statement by a bank, he looked bewildered.

What Ramesh had — and what the bank didn’t ask for — was a simple monthly cash budget he maintained in his notebook: expected inflows, bill payments, raw material purchases, and a weekly buffer for contingencies. It was primitive — but it told a story.

That story was never heard.

1. Cash Budgeting – A Forgotten Tool

Cash budgeting isn’t new. RBI’s guidelines under the Nayak Committee and Tandon Committee once emphasized projected cash flows and inventory cycles.

Yet, over time, banks drifted toward relying on static indicators — audited financials, ITRs, and ratios like:

Current Ratio

DSCR (Debt Service Coverage Ratio)

Working Capital Gap via MPBF (Maximum Permissible Bank Finance)

The shift to documentation over dialogue side lined a critical question :“Does this business have enough cash to sustain itself month-on-month?”

👉 The Nayak Committee (1991) recommended 20% of projected turnover as working capital — inherently demanding cash flow estimation.

👉 RBI’s 2019 MSME Discussion Paper and SIDBI-TransUnion Pulse reports (2023–25) all highlight cash flow-based credit as a necessary future.

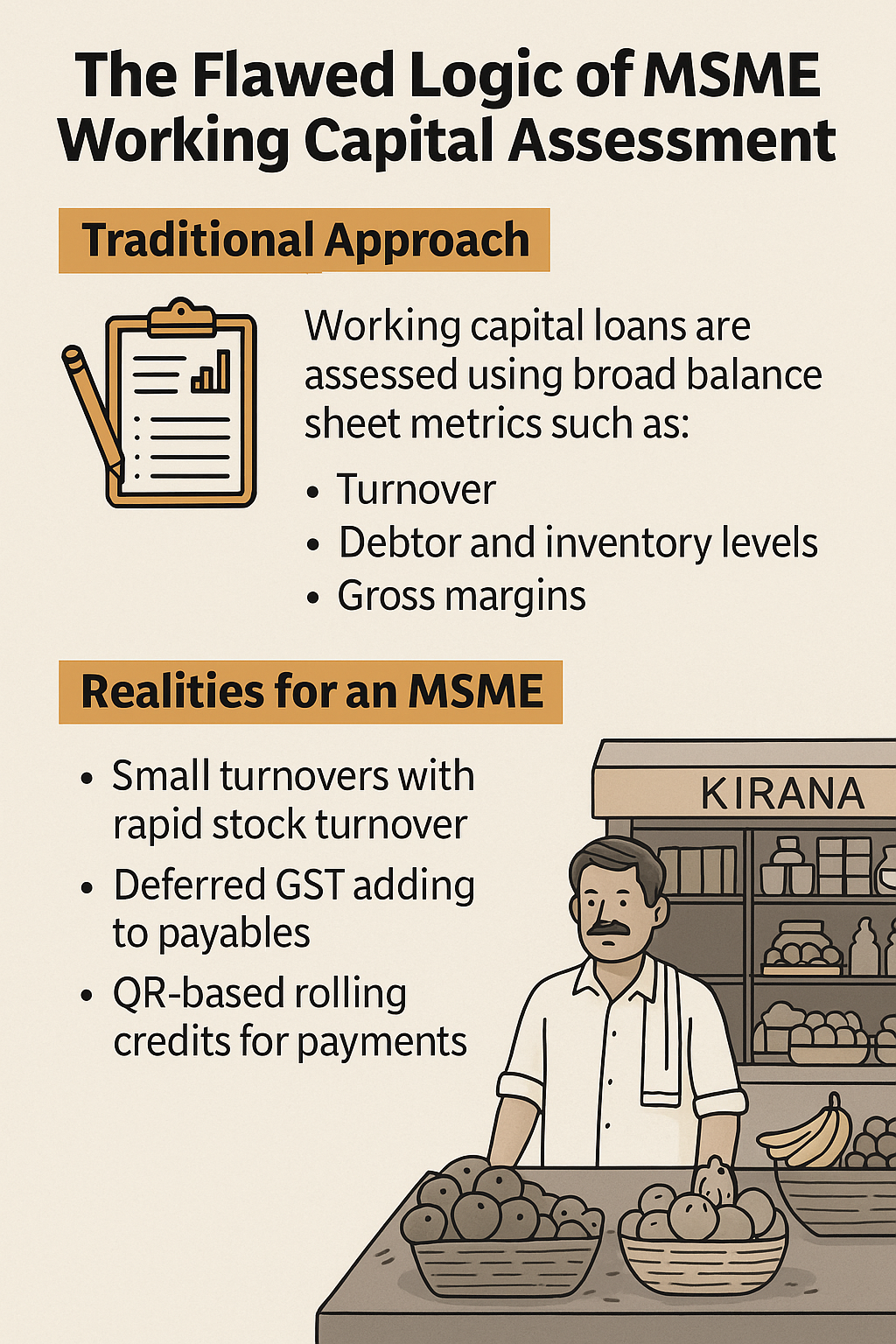

2. Why Cash Budgets Work for MSMEs

Unlike large corporations, MSMEs:

Have variable and seasonal inflows

Make decisions in real-time

Don’t always operate with strict profit accounting

Cash budgets:

Help MSMEs forecast needs and shortfalls

Allow credit officers to see future stress before it manifests

Capture behavioral discipline (e.g., setting aside rent, salaries, EMIs)

Most importantly, they give structure to informal income patterns.

3. Why Are Banks Not Using It Actively?

Volume Pressure: Credit officers have limited time per case

Standardization Issues: No uniform cash budget format for MSMEs

Trust Gap: Self-reported projections are viewed as subjective

Automation Preference: Modern credit models rely on bureau & account scores

Ironically, these same banks are now under pressure to embrace alternate data — without realizing they’ve long had a tool to interpret such data: the cash budget.

4. Bridging the Old and the New

Let’s consider an online vendor who sells organic food on Meesho and receives daily UPI credits. Her ledger may not exist on Tally. But if she submits a monthly cash budget of:

₹1.2 lakh inflow from UPI

₹70K spent on sourcing

₹10K on packaging/delivery

₹15K for family expenses

₹10K toward EMI

... it paints a stronger picture than her previous year’s ITR.

Now if this budget is validated through:

Account Aggregator (AA) data

QR trail analysis

GST-free transaction patterning

... suddenly, a bridge is formed between bankable structure and real-world behavior.

📌 The RBI’s Account Aggregator framework (2021 onward) and the Cash Flow Lending narrative are perfectly aligned with this approach.

5. What Can Be Done Practically?

Stakeholder | Action |

Banks | Build cash budget templates for key MSME types |

MSMEs | Train in basic budgeting — even handwritten |

Fintechs | Create tools to digitize and auto-score budgets |

Regulators | Incentivize early-stage exposure via cash flow |

Conclusion

Cash budgeting isn’t a relic. It’s a revival tool. It gives voice to MSMEs with informal structures, and it provides banks a verified path to underwrite thin-file borrowers without entirely discarding traditional risk models.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.