Beyond Ratios Series

Introduction

Healthy balance sheet ratios often create a dangerous sense of comfort for lenders. But behind glossy numbers, cash flows may be telling a very different story.

Fund Flow Analysis — an often-neglected credit appraisal tool — can unmask whether operations are genuinely generating liquidity or simply inflating assets.

In this episode, we’ll revisit real-world corporate cautionary tales where early fund flow red flags could have changed lending outcomes — and we’ll look at why this method should still be part of every credit officer’s toolkit.

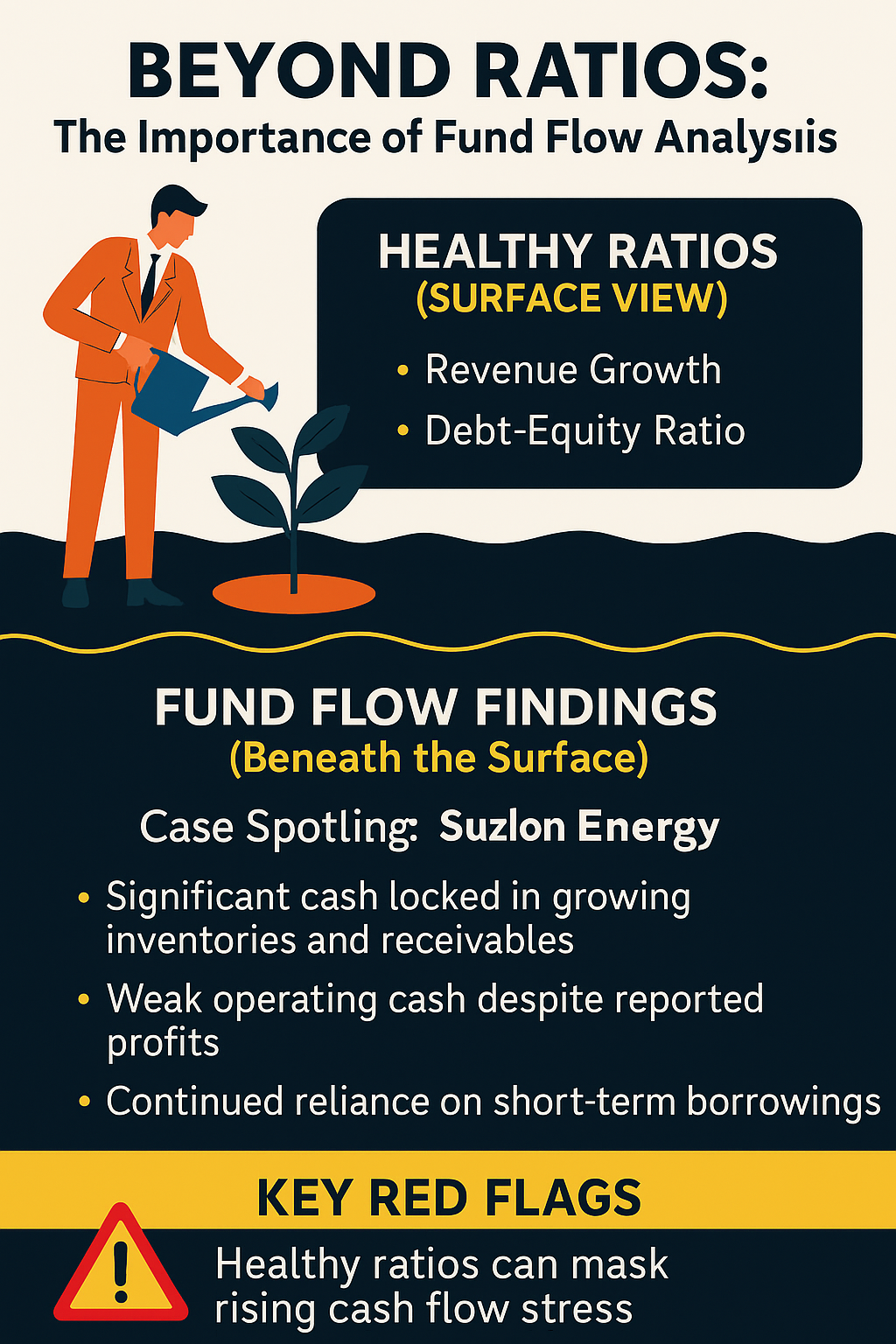

Case Spotlight: Suzlon Energy (2015–2019)

The Ratios: Revenue growth and acceptable debt-equity ratio gave the impression of recovery.

The Fund Flow Reality:

Significant cash locked in rising inventories and receivables

Weak operating cash despite reported profits

Continued reliance on short-term borrowings to meet operational expenses

The Lesson: Healthy ratios do not always mean healthy liquidity — fund flow analysis caught the stress signals years before the debt restructuring.

1. Real-World Examples Where Fund Flows Told the Truth First

IL&FS Crisis (2018)Short-term borrowings repeatedly funded long-term projects. Fund flows showed persistent negative operating cash despite healthy profit reporting.

Source: RBI-appointed Uday Kotak Committee report.

DHFL Default (2019)Large dividend pay outs and rapid loan book growth were debt-funded, while actual repayments lagged.

Source: Grant Thornton forensic audit (Economic Times coverage).

Suzlon Energy (2015–2019)Inventory build-up and rising receivables starved operational cash, even during revenue upticks.

Source: Suzlon annual reports & Business Standard.

Videocon Industries (2018)Asset sales failed to improve liquidity, with fund flows showing sustained cash stress.

Source: NCLT orders & The Hindu Business Line.

2. Why Fund Flow Analysis Is Skipped Today

Many lenders now bypass detailed fund flow preparation because:

Speed pressures in sanctioning (TAT over depth)

Over-reliance on automated scoring and ratios

Perception that fund flow is only for large corporates

This “efficiency over prudence” mindset has led to loans being sanctioned without fully understanding liquidity movement.

3. What Credit Officers Should Look For

In any mid- to large-ticket corporate or MSME appraisal:

Check whether profit translates into operating cash

Look for sustained increases in receivables or inventory without matching sales

Identify reliance on short-term borrowing for long-term needs

Spot large capital expenditure without internal accrual support

Conclusion

Fund flow analysis is not a luxury; it’s a necessity. For corporates and MSMEs alike, it bridges the gap between accounting ratios and actual liquidity health.

Ignoring it is like diagnosing a patient solely from a blood report without checking vital signs — you may miss the crisis until it’s too late.

Disclaimer:All company examples are based on publicly available information from credible news and regulatory sources. They are presented solely for educational purposes in the context of credit risk awareness and not as a comment on current financial health or creditworthiness.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.