Section 94, Sequencing Power, and the New Insolvency Reality

The branch received a letter.

It was formally worded. Procedural. Calm.

The personal guarantor had filed an application under Section 94 of the Insolvency and Bankruptcy Code (IBC) before the NCLT.

An interim moratorium under Section 96 had commenced. Proceedings in respect of the debt stood stayed.

The branch team read it twice.

This was not a visibly stressed account.

Interest was being serviced.There was no SMA classification. No legal notice had been issued. No confrontation was underway.

Routine review meetings had taken place. Financial statements were submitted. Monitoring was ongoing.

And yet, insolvency proceedings had already begun. The surprise was not legal. It was strategic.

Insolvency Without Collapse (Section 94)

Banking instinct assumes insolvency follows default. Escalation. Breakdown.

Under Part III of the IBC, that sequencing is not mandatory.

Section 94 permits a personal guarantor to initiate insolvency proceedings. Section 96 provides that interim moratorium begins from the date of application.

Not admission. Not scrutiny. Filing.

This statutory structure was upheld by the Supreme Court in Dilip B. Jiwrajka v. Union of India (2023 SCC OnLine SC 1582), affirming that interim moratorium under Section 96 is triggered upon filing of an application under Section 94 or 95.

That distinction changes recovery psychology.

Insolvency can precede enforcement.

And when insolvency precedes enforcement, leverage shifts quietly.

The Asymmetry No One Talks About

The branch was monitoring financial performance.

The guarantor was monitoring procedural positioning.

There is no statutory requirement for advance notice before filing under Section 94.

The guarantor knows when filing is being considered.

The bank does not.

This informational asymmetry is the core issue.

Not misuse.

Not illegality.

Timing.

The Structural Incentive Embedded in Law

Section 94 is not a loophole. It is a statutory right.

But legal design shapes behaviour.

When interim protection begins immediately upon filing, filing timing becomes consequential.

If enforcement has not yet begun, filing alters the procedural battlefield before the first move is made.

This is not an allegation of systemic abuse.

It is recognition that incentives influence conduct.

And institutions must adapt to incentives.

The National Pattern: This Is Not Isolated

Data from the Insolvency and Bankruptcy Board of India (IBBI) illustrates the scale:

As of 31 March 2024, total personal guarantor applications stood at 2,800 (IBBI Annual Report 2023–24).

As of 30 September 2025, the number rose to 4,292, including 640 debtor-initiated applications under Section 94 (IBBI Data Compilation, September 2025).

An increase of nearly 1,500 filings in approximately 18 months.

Six hundred and forty proactive debtor filings.

This is not sporadic.

It reflects behavioural adoption of the framework.

When Sequence Inverts

Traditional recovery arc:

Default → Notice → Guarantee Invocation → Enforcement → Insolvency.

Emerging arc:

Anticipation → Filing → Interim Moratorium → Process.

This inversion changes leverage.

Recovery moves from execution mode to procedural participation mode.

The bank shifts from controlling the timeline to responding within it.

That shift is subtle — but profound.

Judicial Scrutiny Is Emerging

Recent appellate developments indicate that courts are not blind to timing dynamics.

In early 2026, the NCLAT (Delhi Bench) dismissed a repeated Section 94 application, observing that it appeared intended to defeat ongoing SARFAESI recovery proceedings. The tribunal refused to allow procedural mechanisms to become instruments of delay.

This signals something important.

The ecosystem itself is evolving.

The conversation is moving from:

“Can Section 94 be filed?”

to

“How is Section 94 being used in practice?”

That distinction marks maturity — and scrutiny.

The Post-Facto Discovery Reality

After filing, recovery teams often turn to asset history:

Transfers. Encumbrances. Structural adjustments. Trust formations. Ownership shifts.

The IBC provides tools to examine preferential or undervalued transactions. But those processes require evidence, time, and adjudication.

The discomfort is rarely immediate illegality.

It is sequencing disadvantage.

By the time scrutiny begins, the procedural frame has shifted.

What This Means for Stakeholders

This shift is not theoretical. It is operational.

For Branch & Relationship Managers

“Interest serviced” no longer guarantees “no procedural risk.”Soft stress signals deserve earlier escalation.

For Recovery & Legal Teams

Speed and sequencing discipline are strategic tools. Section 95 creditor filings must be evaluated proactively, not reactively.

For Credit & Risk Functions

Guarantor exposure monitoring must extend beyond annual declarations. Legal timing vulnerability must enter early warning systems.

For Senior Management

Integrated credit-legal coordination is no longer optional. When filings grow from 2,800 to 4,292 in 18 months, behavioural shifts are underway.

The Missing Conversation

There is one more dimension we rarely discuss.

Banks compete. They should.

Competition sharpens pricing, service, and efficiency.

But insolvency risk is not competitive.

It is systemic.

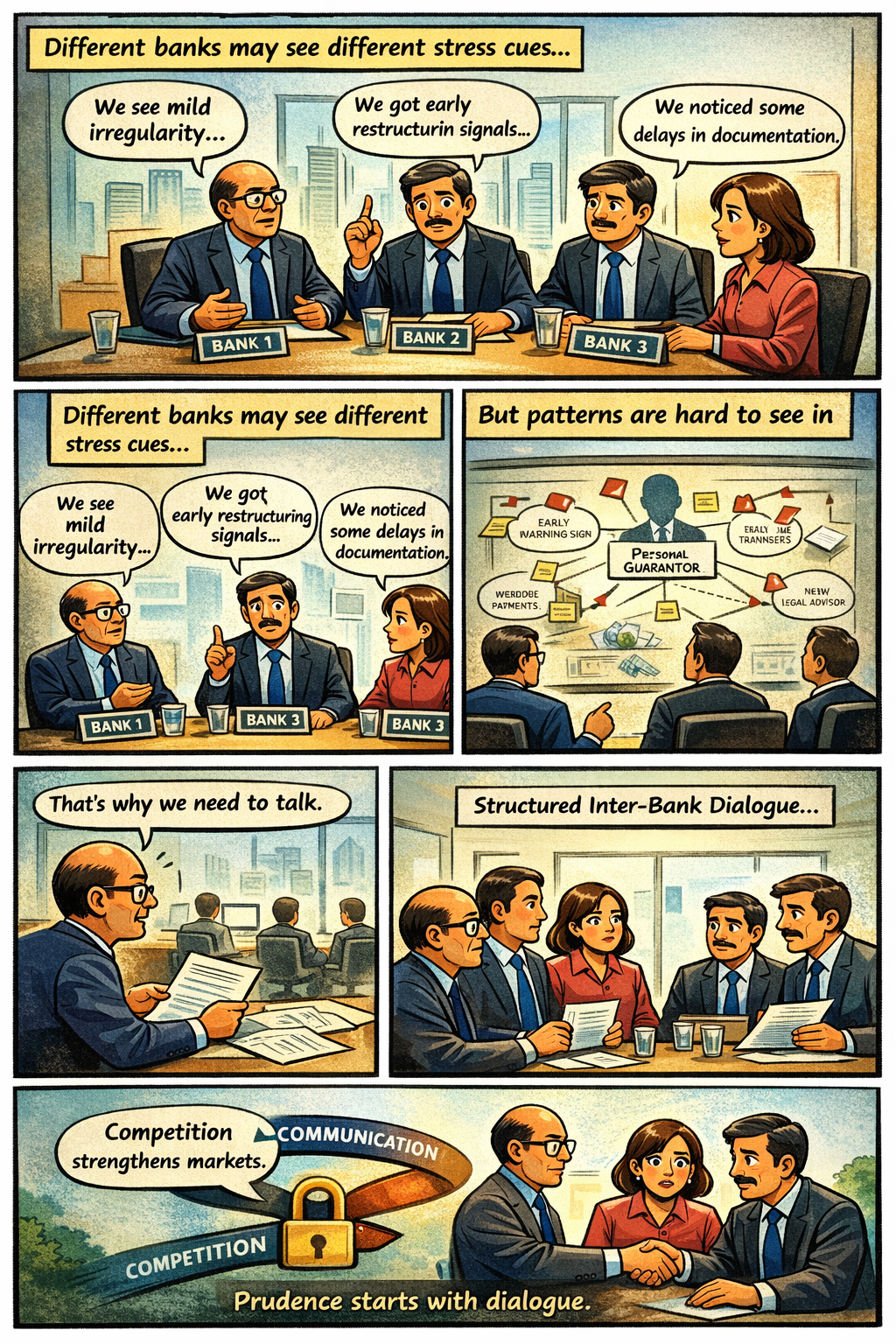

When a personal guarantor files under Section 94, it often affects multiple lenders.

One bank may observe mild irregularity.

Another may see early restructuring signals.

A third may detect documentation delays.

Individually, none of these may appear alarming.

Collectively, they may form a pattern.

But patterns remain invisible when information is siloed.

This is not a call for collusion.

It is a call for prudential awareness.

Structured, lawful inter-bank dialogue — particularly in consortium or multi-banking exposures — can:

Reveal emerging stress signals.

Detect early legal positioning.

Avoid procedural surprise.

Competition strengthens markets.

Communication strengthens systems.

Not Misuse — But Evolution

Many Section 94 filings reflect genuine distress.

There is no empirical dataset proving systemic abuse.

But rising debtor-initiated filings and judicial scrutiny of repeated applications indicate growing sophistication in how the framework is used.

Legal systems evolve.

Participants learn.

Institutions must learn faster.

The Real Lesson

The branch that received the letter was not careless.

It was operating under traditional recovery assumptions.

Those assumptions now require recalibration.

The bank was monitoring financial metrics.

The guarantor was monitoring procedural leverage.

In modern insolvency dynamics, advantage lies not only in collateral strength — but in sequencing awareness.

Insolvency may no longer follow visible collapse.

It may arrive quietly. One letter at a time.

And institutions that anticipate that possibility will operate from strength — not surprise.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.