It was a frenzied Monday morning, towards the month end. As I quickly ran through the figures.

So what is surprising here ?

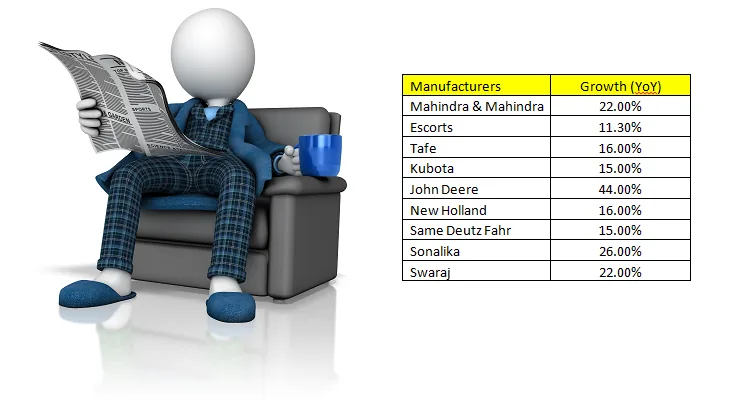

The average usance / work based growth is about 5-6%, and a stretch to about 8%. So manufacturers who are typically between 8 – 11 % will see consistency in their growth. What about the others ? So how safe is the growth we are experiencing ?

The Financier Dilemma :

Banks need to fulfill their PSL Obligations (Priority Sector Lending). One segment of which is Farm Equipments. While the effort is made by Banks to achieve their PSL, there is invariably the shortfall which is bridged by Buy-outs. This is provided by the NBFCs.

The latest trend with NBFCs who are focusing on Farm Equipments, is to increase their capacities by borrowing through CP and CDs. These are promissory notes for short periods. NBFCs do seasonal stretching to cope up with demand from the banks.

In a bid to do this, the cost of capital / funds for these NBFCs have therefore pushed up rates from 25 bps to about 150 bps. This is laced with lot of offers , deals, schemes, payouts, commissions etc.

Yet, considering that the buyout takes places within 6 months of CP / CD Borrowing, the asset liability mismatch is not wide.

This also drives the financier into a frenzy to balance the time frames in which the loan book is raised.

The Government Catalyst :

Each state government has been doing its best in offering subsidies and sops to farmers primarily to make farmers embrace mechanization, and enhance productivity.

However, largely, the governance of each of these subsidies, has left a lot in expectations. In majority of the cases, bad governance has led to misuse of these schemes, which are otherwise very noble in their intentions.

What could have spurred mechanization, and growth in GDP, has been scuttled to mere enhancement of income to a select few.

What could have been the much required catalyst towards growth, leaves us thirsting for better. But why ?

Let’s take the simple and apparent ones :

Subsidy Utilization

- Deferred / Stage Disbursed Subsidies became Single Point Upfront Disbursement Subsidy. Yet coordination between Subsidy and RTO was never tied in to arrest Phantom Purchases.

- People started making “Subsidy Usance” the main business. Farm Equipments are purchased under subsidy , subsidy is availed and within 6 months sold to another user.

- The fact that this subsidy was supposed to spur economic activity, and the facte that these subsidies are given from the tax payers pool. Neither is economic activity spurred nor does the tax payers woes end.

Subsidy Governance

- Corruption is rampant, and almost amounts up to 50-60% of the subsidy is spent on getting the permit and subsidy executed.

- This in turn gets the customer pushing the dealer and the manufacturers, to adjust and re-align pricing. The pricing pressure increases the number of variants. So one particular model , 3 years back would have had 2 variants, and has 10 variants now. This is to suit the pricing requirement of the customers. The customer recognizes his product with the model number and does not delve deep enough on the variants.

Concentration of Subsidies

Tractors has a separate subsidy, Implements have separate subsidies, Harvesters have different subsidy schemes. The database gaps between each of these subsidy scheme are made use of royally. So there is no group / family level subsidy exposure monitoring. Within the same family of 6 people, subsidies exist in the name of 4, and are operated by the same person.

So the used market gets hit.

a. Average usance of a tractor having 15 year Engineering Life, 8 year Economic Life, is churned in 2 years.

b. Prices are determined by Demand and Supply, and not by the intrinsic value of the vehicle or its capabilities.

The Vision of Manufacturers :

There used to times when the focus was on what the product and what the product could deliver. However, the focus has shifted from product and capability to Pricing, Discounts, Exchange Values etc.

Manufacturers offer credit, inventory credit based on the dealer capital and constitution. Many of them have floated separate finance companies and fund dealers through this arm, much beyond his capability.

This ensures :

(a) That the Dealer drives consistent sale to avoid being charged excessively.

(b) That the Dealer has no time to do base ground work and develop market share in his locality of strength.

(c) That the dealers focus on selling rather than marketing their product. Selling the concept of tractor is required. Yet what is marketed is a product.

The approach should be utility basis rather than offer driven / product driven. One of the key observations is that the number of tractors in the location has gone from about 1 tractor for every 160 Hectares to about 1 tractor for every 35 Hectares. About four fold increase in the tractor density, and yet overall mechanization has seen a meager 1.8% growth.

The Dealer

The dealers realized a simple street arithmetic. As long as their tractors were seen on the roads, they still had a chance. So the approach at the sale point changed from unit based margins to volume based margins.

If the dealer was selling at Rs. 50000/- Margin per unit, and did 5 units, he would now do 25 units with Rs. 10000/- margin. The overall return may be the same, and yet the market share is higher.

This market share becomes the key USP and marketing point, to scale and market product with different variants and margins. Customization begins.

The Reality

The hard reality is that the net irrigatable land is about 52%. Of this 55 - 60% is Paddy. Paddy income alone is insufficient to service all the liabilities of the farmer.

The farmer therefore enhances his operations, and includes hiring, and contractual work, which becomes the basis for his repayment.

As a customer / farmer, they have to accept that the margins per acre of paddy is thin.

The financier has to accept that categorizing customers as AGRI does not mean, that agri income has to be the only source of work. Allowing PSL categorizations to govern / influence customer selection and credit assessment is sure shot method to grow NPA.

The Government has to connect – Execution – Connecting Farming Activities with Subsidy - Governance. Today it is “easy money”. Subsidy to GDP Growth Ratio has to be linked.

Manufacturers need to restrict growth in units to a maximum of 10 – 12%. Growth greater than this can be harmful.

A holistic growth is sustained growth. We currently seem to inevitably ride the bubble. Yet how long can the bubble be kept up ? Till we wait for the next low cycle of weather, and choose to waiver these farm equipment loans too ? Where is it that we take responsibility for balanced growth ?

If a dealer cheats on us today, we as financiers and manufacturers educated him. If a manufacturer puts pressure beyond reason, we as dealers accepted and allowed him to ride us. If as customer, if subsidy is misused, the focus was not on effective subsidy usance but the vote bank that it garnered. We ourselves are to blame for not taking actions in our respective spheres of influence. We have directly / indirectly fuelled the tractorization rather than mechanization ! “When will the bubble burst ?” is the question on everyone’s mind…. Where do we start ? What should be the Early Warning Indicators ?

(Views expressed herein are personal and a mere analysis as experienced first hand, and do not represent any company or corporate entity.)

Archive note

This essay was restored from Vivek Krishnan’s LinkedIn archive. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.