The “Pre-Owned” vehicles have always been a special segment !! To the world of tractors this is nothing new either. A colleague of mine was exchanging notes with me on the various facets involved in Used / Pre-Owned Tractors. The key link as we discussed, turned out to be the valuation report tossed up by a professional valuer. Both of us had our humble beginnings in Valuations, and hence we progressed to dissect this world.

This is more from what to expect from a Valuation Report. This is more like what we would have done as part of Valuation of a Used Tractor / Pre-Owned Tractor.

A Note : To all my brethren from the Valuation world. This blog is more like explaining the blood reports – just to take a simili. Just because these nuances are discussed, doesn’t mean that any of us would perform this task ourselves. It still requires a professional. This only highlights the lovely work you bring to the table !

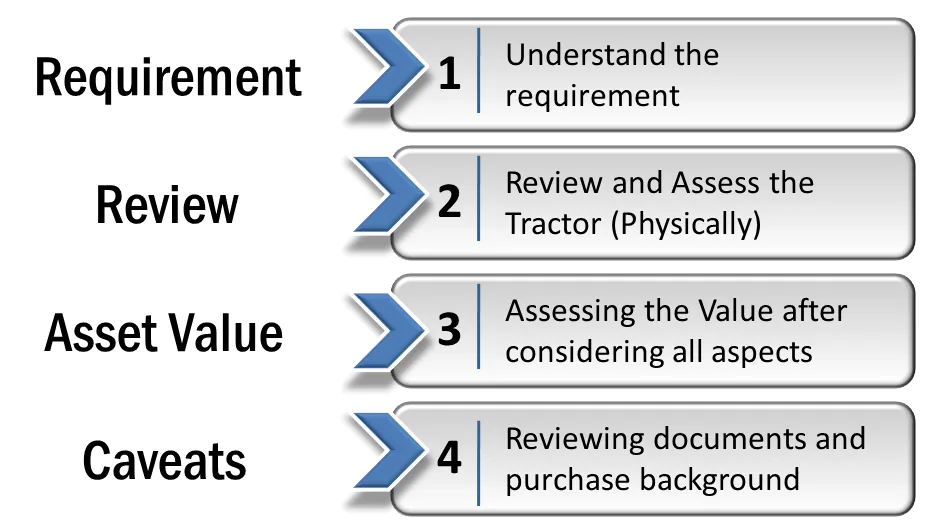

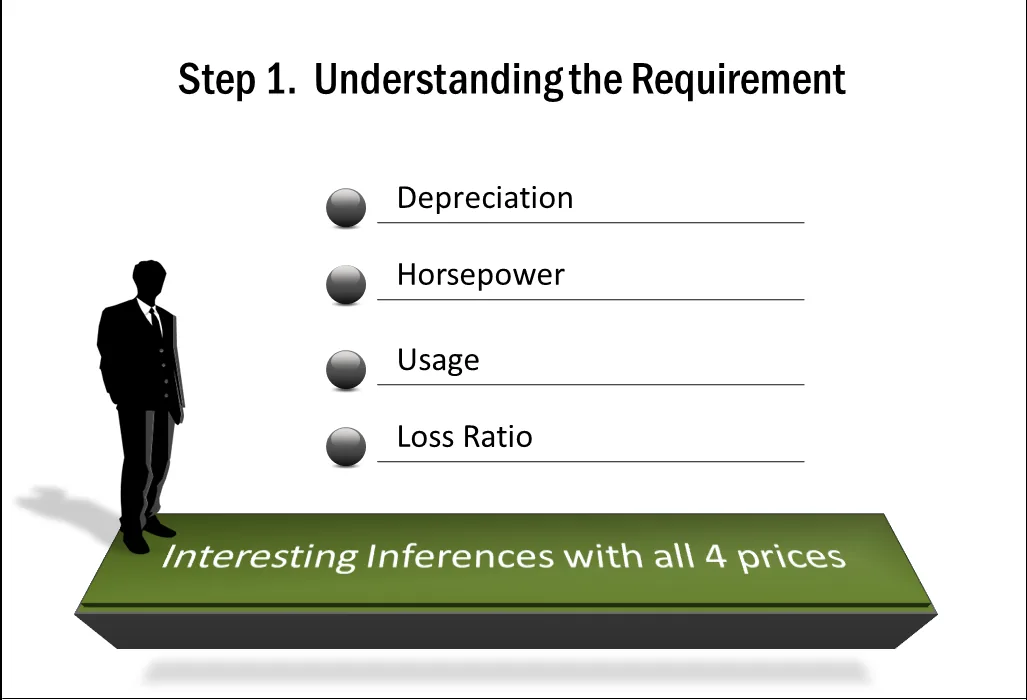

STEP 1 : UNDERSTANDING THE REQUIREMENT :

One of the first things that a valuer does is to ascertain the perspective from which the valuation is being done.

- Seller’s Price : Price that a seller would get selling the model being evaluated

- Buyer’s Price : Price that a buyer would need to pay for the model being evaluated

- Auction Price : Price that a Financier would get considering tractor condition

- Distress Sale : Worst Case Scenario price that either Financier / Seller would get if a Time tag is attached to the sale. (Short Term).

These are 4 different prices of the SAME Model. My Mentors in Valuation taught me that a valuation report should cover all aspects. These value systems have since evolved to customized approaches in valuation reports being presented.

So what inference could financiers draw if all 4 were given part of the valuation report ?

1. The highest rate would be the Buyer’s Price

2. The Second highest would be the Seller’s Price

3. The Third would be Auction Price

4. The last of them would be Distress sale.

So price volatility in case of a sale is known. Interesting Facets that emerge

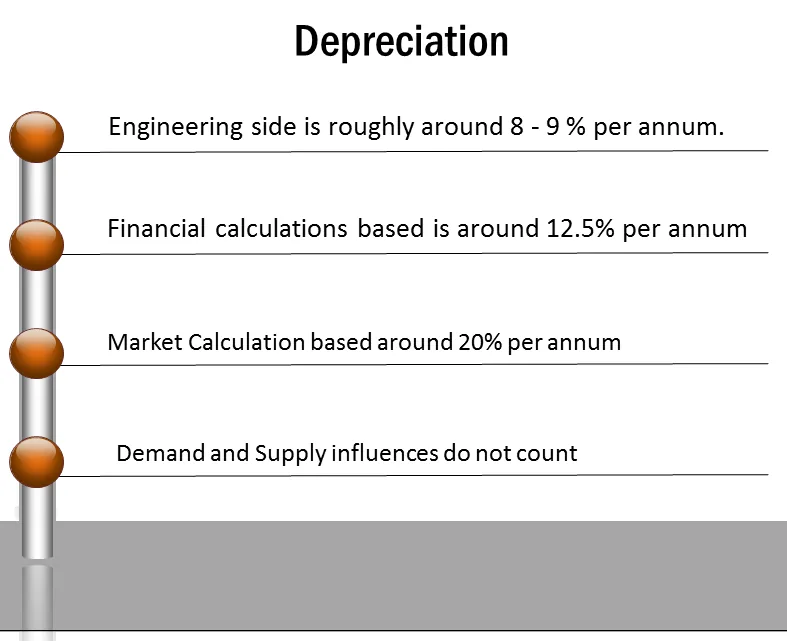

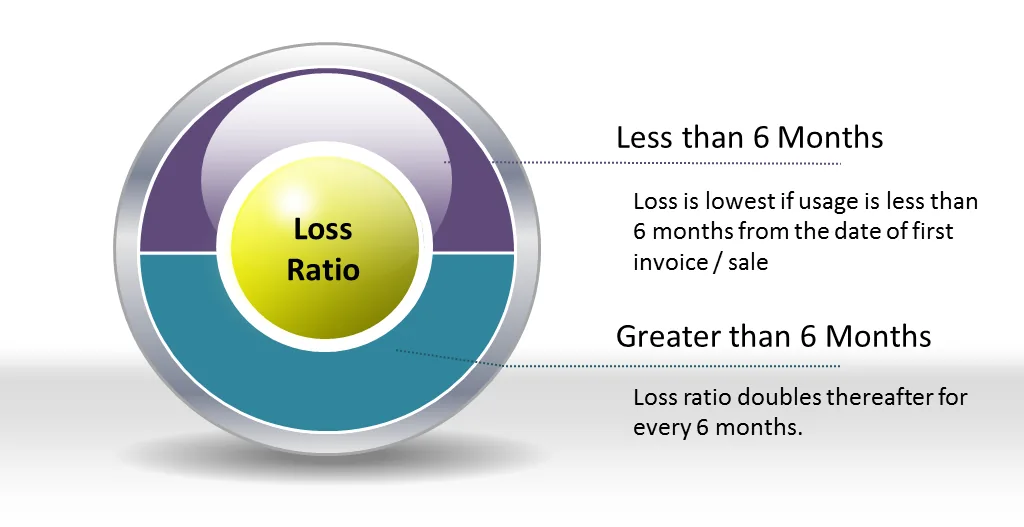

First 6 months – Normal Loss / Wear & Tear Loss / Usage Loss. Next 6 months - Loss is equal to 1 year and so on.

So, the gap between installments / dues and the market value of the underlying asset are galloping at two different paces.

Unless a STOP LOSS mechanism is pulled into place in time, invariably these scenarios are taken over by Distress Sale Pricing.

As a financier, in the current day context, keeping tab of the value of the underlying security and marking the same to my portfolio and its impact is the most critical function of the Valuation Report.

From a Valuer’s aspect, Valuation done for a financier therefore has to cover any / all perspectives that will impact the Loss Ratio, or depreciate the asset at a faster rate than depletion of its outstanding loan dues / collateral value requirement. In Warehouse Receipt Funding or a Jewel Loan, we could do something like a MARGIN CALLING to bridge this gap. For Tractors, this possibility is almost nil.

STEP 2 : REVIEW OF THE TRACTOR :

This has been the most interesting part of valuations that we have been part of. Every time, there were new learnings. I was a commerce graduate, and yet I used to move from Vehicle to Vehicle with child like curiosity trying to apply nuances that we were taught.

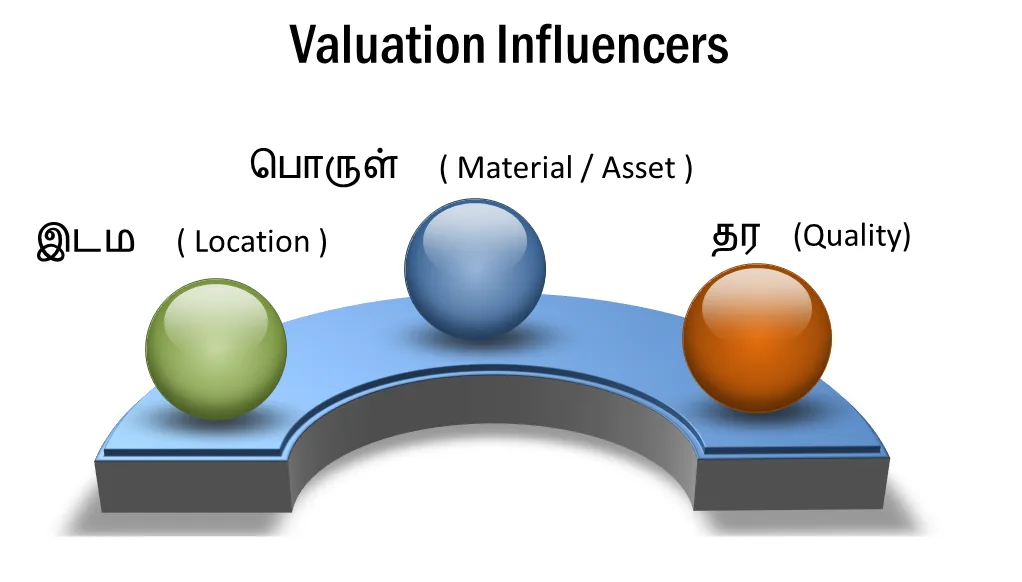

In valuation, under this criteria, we were taught to observe 3 aspects. I quote this in Tamizh, (though Tamizh is as much a foreign language to me – I only know to speak Tamizh), because the words stand etched that way and the beauty of the language does the magic.

Location :

Where the asset is currently located and being reviewed will make an impact on the valuation.

One of the first instructions that we are made to give our customers is not to shift the vehicle for the sake of inspection / verification and the asset was to be valued at the place of purchase. It could be seller’s fields, godown, shop, residence, or auction or repossession yard.

The location and maintenance plays a very critical role. Depreciations soared as high as 18% based on location especially if Auction or Repossession Yards.

Asset :

The Model has a very unique role to play. While many schools of thought have argued the same to be perceptions of vested groups, we have other patterns emerging. Let us for a minute assume that the vested group perspective is true. End of the day, what matters is given the worst case scenario, what will buyer pay for the given model ?

So the brand which is perceived better, is evidenced by :

(a) Purchases in the past

(b) Stock of Parts, Service Centers, Mechanics in the locality

(c) Implement and Horsepower used in the locality for different types of work.

Quality :

This is very specific to the asset being evaluated. Within Model and Brand, values have known to differ depending on the checks and responses to :

(a) Cold Start Test

(b) Tyre Lug Test

(c) Noise, Smoke and Hydraulics Check

(d) Damages and Repairs Check

This gives an idea of the investments that the buyer would need to put in after purchase of the asset, which, based on time frames involved, will have differential discounting factors.

The biggest NO-NO in tractor valuation is never to go by physical and superficial appearance of the vehicle. While good looking tractors are indicators of good maintenance, they could also be indicators of low use / stationary use. Appearances in tractor valuations would be deceptive and cannot be taken up like how we do for Cars / LMVs / SUVs.

Step 3 : EVALUATION / ASSESSING THE VALUE

Valuation of the Tractor is one of most challenging. If the value predicted is not received, the valuer is questioned, and many financiers have an experiential mapping of valuers. Valuer A – 80% of whatever he gives, Valuer B – 50% of whatever he gives.

This defeats the purpose. Yet what is challenging is that our brothers in finance have not understood

(a) Value on scientific norms is what we call INTRINSIC VALUE of the Asset.

(b) The market cartels and bids a lower price than the INTRINSIC VALUE.

(c) However, when the bidder sells the tractor again, it will be higher than the INTRINSIC VALUE.

So the question of the INTRINSIC Value not being honoured does not arise. Who finally benefits ? It is strategy.

When an insurer takes premium for an IDV we pay.

When a sale occurs and when the buyer pays lower than IDV, do we question the Insurance company as to why he took a higher IDV ? So why question the valuation ?

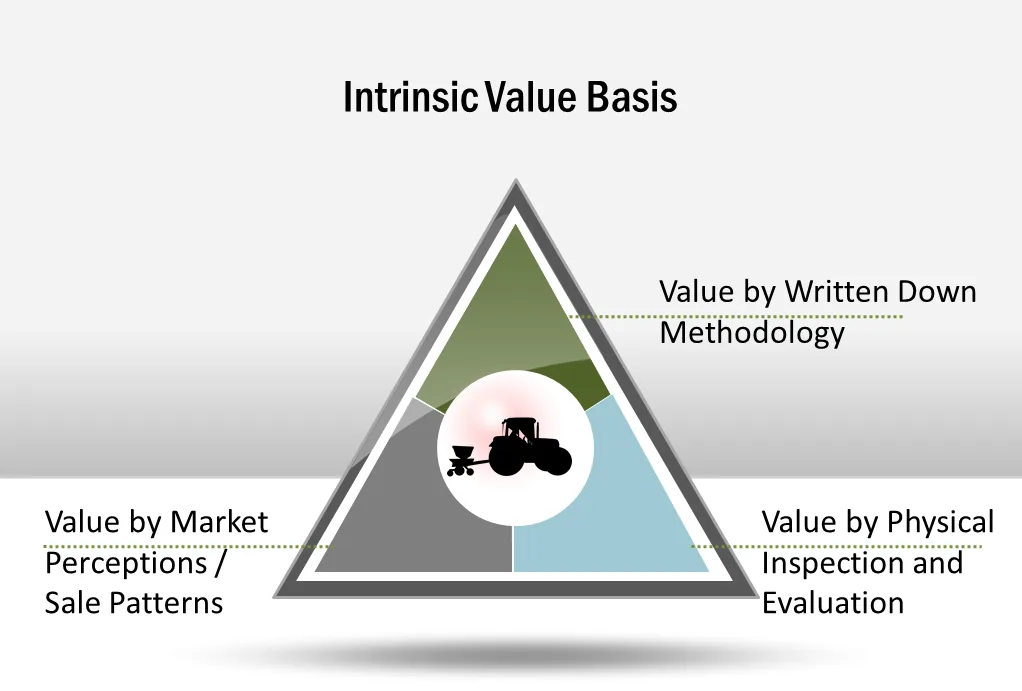

Intrinsic Values are derived by crossing 3 prices :

(a) Value by the Written Down Methodology

(b) Value by Market Perception / Sale Patterns

(c) Value by physical inspection and evaluation

While (a) and (c) are given higher weightages, (b) is factored as a deduction from (a) and (c). So lower of (a) or (c) is taken as intrinsic value.

Intrinsic value will definitely be received by the final seller. It may not be the financier. It is best that the financier looks to hedge his position to the best, and exit in case of financier induced sale.

STEP 4 : Document Evaluation :

This is where many of my valuation brethren from the current generation falter. Document Evaluation for a Tractor is not just about RC, Invoice and Insurance.

It has to cover all aspects that will impact purchase or sale of the asset. For example, in some states like Karnataka, an asset funded under Subsidy cannot be transferred for a period of 5 years. While in some other states it is not explicit, and yet the enforcement clauses mention that in case the asset is transferred to another owner, the subsidies so given is recoverable by the Government.

There would be cases wherein the Manufacturing year actually is 2015 and yet the RC mentions the same as 2016.

A Valuation Report is expected to give such insights to aid purchasers of where they would be or what lies in store for them. This in turn would cover all stakeholders - Be it a Seller, Buyer, Financier , or Auctioneer.

Archive note

This essay was restored from Vivek Krishnan’s LinkedIn archive. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.