As has been my experience, in my recent years of my career, the start point for any investigation, Underwriting, or process has been to check if all facts were correctly elicited and recorded and then check for misrepresentation.

This brought forth an importance of the principle of TRUTH BIAS in the whole system. This blog is a journey of the path, my experiences have taken, and the depth to which this principle is entrenched.

“The most natural thing for a man is to speak the truth” – by C Rajagopalachari

In the world of Agri Finance, where I hail from, this is the key mantra or the basis for a number of initiatives taken by my brethren in the same field including myself.

Looked at it from a different perspective, many would say, that the choice to adopt this mantra is a conscious one. So what do we mean by this TRUTH BIAS.

“The tendency to assume, in the absence of evidence, that interaction partners are speaking the truth” – This is the bias that the human instinct has towards truth.

If we look at the activities of Field Investigation, Sourcing, Credit Underwriting, Fraud Evaluations, this principle is at work

- The Sourcing Team believes that the Customer is uttering the Truth, unless the sourcing official evidences something to the contrary.

- Field Investigation relies on the principle that Customers are uttering the truth, and needs help in corroborating this truth in a metric / algorithmic / logical pattern of data points. This report plays a vital role Non-declaration of information and materiality.

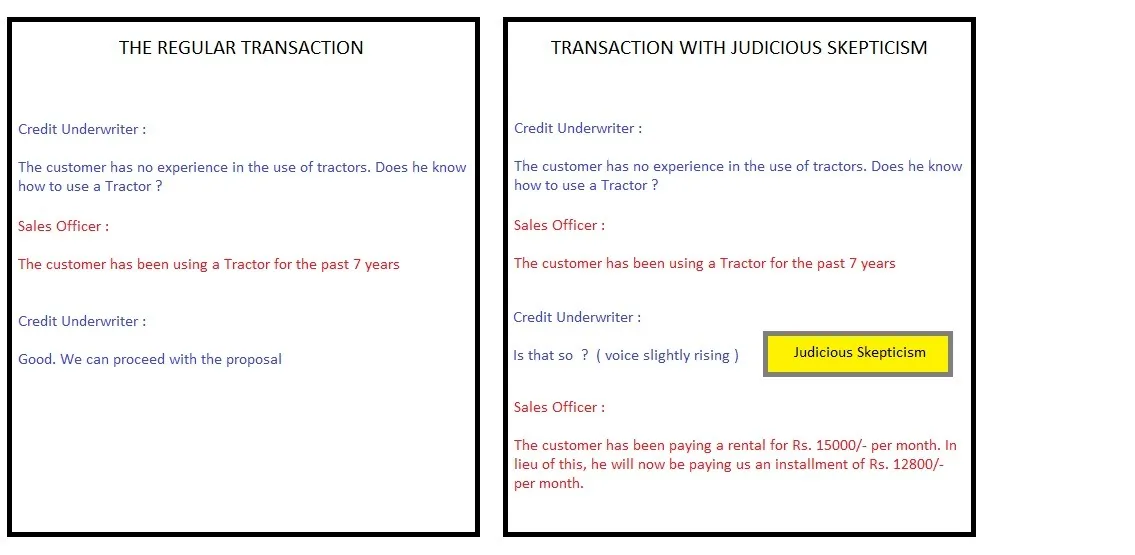

- Credit Underwriting seeks to ascertain the need of the customer and validates his ability to support his need. The start hypothesis for a sound underwriting practice is to adopt judicious skepticism, which aids in gathering information about the intention of the customer.

Specifically seen from the Rural Markets context, the belief that the vile ways of Urban Lifestyles, and a induction of negativity in attitudes has not taken place in the Rural side of India. Hence, the belief is that Rural India adopts truth relatively, more naturally and is more instinctive. While this is definitely debatable, we cannot shy away from the fact that almost all financiers have no choice but to adopt this as a start-point for our business. So every attempt of a Credit Underwriting, RCU, Risk Modelling has a limitation in assessing the real image of a prospective.

This was most felt earliest in the field of Insurance Underwriting, and today is known as the Doctrine of Utmost Good Faith (uberrimae fidei - Latin).

So the essential start point is an honest declaration of material information. This had to have a context. Thus was born a formatted application form, wherein a declaration clause is introduced in most application forms, where one party formally seeks to contract / engage with another for pre-specified considerations, based on declared facts from either party to the contract.

DECLARATION. I declare that to the best of my knowledge the information given is true and correct. I understand that inaccurate, misleading or untrue ...

The materiality of the information and the usage of this principle is governed by many statutes like

· Sec 45 of the Insurance Act, 1938

· Sec 52 of the Indian Penal Code

· Sec 223 of the Contract Act, 1872

So the entire edifice of a transaction starts from a truthful declaration of information.

There have been very many interesting cases in the corporate world, circling around the declaration of TRUTH - presence or lack of it.

This has also brought forth perspectives on declarations from all respective parties to a contract. So let’s look at an example:

- Customer not declaring in a loan application that he has borrowed from a local money-lender.

In this context

- The Customer should have explicitly said NO EXISTING LOANS, to hold him / her accountable.

- The mere absence or ambiguous answer of “NO” would be insufficient to proceed against the customer.

2. The Financier enforcing a clause written in fine print, which has been signed off by the customer.

In this context

- Based on a recent ruling, the principle of CAVEAT VENDITOR prevails, where it is the duty of the financier to explicitly and in good faith explain the clause to the customer.

- The fact that the customer was explicitly informed on this clause needs to be proved.

The entire objective is to prove that transactions were honest, fair and truthful.

While as financiers, we may look at the transactions and what went wrong, the ideal start-point is to validate the veracity of information as at the date of application / declaration.

In many cases, finance companies have failed to prove that the customer did not give material information, except in cases like health insurance, where common-man logic is used and is backed by medical science to prove breach of good faith declaration.

There have been very many treatises with the start point as TRUTH BIAS, each of which dealt of psychology of people. Yet many like me get to know its full purport when a transaction hits a dispute.

- Irrespective of whether it is Sales, Operations, Credit or Collections Process, all have its genesis from information that is declared by the borrower, in the Rural Finance perspective.

- Declared information has to be validated on best effort wherein reasonable care or reasonable investigation has to be done by the financier / counter-party, who rely on the declared information.

If material information is not declared by an applicant, the law will seek to ascertain if due diligence process was conducted. The law will also seek to understand the efficiency of the due diligence as a process, before it even proceeds to act on the declaration.

As a customer, many a time we would have signed off on blank forms when applying for a loan. We too expect that the financier will be fair and truthful. Even that is an act based on TRUTH BIAS.

According to the research treatise of LIE-SPOTTING by Dr. Pamela Myers, she zeros down the need for deception to be adopted for :

- To obtain a reward that's not otherwise easily attainable.

- To gain advantage over another person or situation.

- To create a positive impression and win the admiration of others.

- To exercise powers over others by controlling information.

Even if the material gains are not there, deception could be adopted even in the following circumstances

- To avoid being punished or to avoid embarrassment.

- To protect another person from being punished.

- To protect yourself from the threat of physical or emotional harm.

- To get out of an awkward social situation.

- To maintain privacy.

These are just perspectives which have helped me tremendously from the legal perspective, and hoped it would provide an insight into the understanding of truth bias as a principle and how it can be applied.

Archive note

This essay was restored from Vivek Krishnan’s LinkedIn archive. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.