The Incredible Journey of a Gold Bar: From Metal to Ornament

- Dec 11, 2025

- 10 min read

Updated: Dec 12, 2025

Jewellery Business Series — Episode 1

A story of fire, skill, memory… and money.

If you walk into a jewellery workshop before sunrise, you will hear it before you see it. The hiss of the furnace. The metallic tap of a hammer. The whir of a rolling mill waking up for the day.

On the table lies a simple 24K gold bar—no shine, no personality, no beauty.Just a piece of metal.

But in the next few hours, it will become something else entirely.

1. The First Transformation — Fire & Purity

The bar is melted, purified, and alloyed. Gold is too soft to hold shape, so copper and silver enter the story. This single choice—21K or 22K or 18K—decides what the ornament can become.

Even at this early stage, a jeweller is already calculating:

Wastage

Karat variation

Recovery cost

Labour needed

Final margin

The business starts long before beauty appears.

2. The Metal Splits Into Many Futures

✨ The Ingot: Where All Journeys Begin

Once alloyed, the molten gold settles…The glow fades…And a dull, heavy ingot emerges — quiet, unassuming, yet full of destiny.

From this single block, paths diverge:

Some ingots become bangles — requiring ductility

Some become chains — needing tensile strength

Some become pendants — where design & stone-setting dominate

Some become filigree — requiring extreme softness and precision

Some become plain-gold inventory — the banker’s favourite

Some become stone-heavy designs — the auditor’s nightmare

Every ornament belongs to a family, a bucket, a behaviour pattern.

💠 Bankers rarely see this.💠 Karigars never forget it.

Because the way an ingot will behave in melting, rolling, drawing, casting, stone-setting, polishing……is already decided inside that alloy.

And for lenders, this matters: Collateral quality doesn’t begin at the showcase — it begins in the crucible.

3. The Karigar’s Touch: Where Metal Learns to Become Art

This is where the real magic begins — far from the glitter of the showroom and deeper than any stock statement can capture.

Here, in a modest workshop with a single bright lamp, gold is not yet ornament. It is a living metal being coaxed, persuaded, and disciplined into beauty.

Gold is beaten until it learns strength.

Rolled until it yields uniformity.

Stretched until elasticity meets its limit.

Twisted until the design breathes.

Soldered until joints become invisible.

Engraved until personality emerges.

Polished until the surface remembers light.

And through every step, the karigar reads the metal like a language.

He knows, without needing a single instrument:

Which alloy will crack when pushed a fraction too far

Which sheet will tear under the rolling mill because the mix was imperfect

Which wire will break during twisting because the ductility was misjudged

Which design will hold stones securely and which will betray the setter

Which piece will shine after polishing and which will stubbornly stay dull

Which ornament will melt cleanly and return purity without surprises

Which stock will confuse a banker, because its weight and true value do not live in the same place

This wisdom cannot be taught in classrooms. It lives in the fingertips that have shaped gold for decades. It grows in the rhythmic blow of the hammer, the controlled hiss of the flame, the way the karigar tilts his head to judge colour, depth, hardness, and possibility.

Bankers rarely see this. Karigars never forget it.

And somewhere between these two worlds — between the artisan who understands metal and the financier who understands numbers —lies the truth about jewellery lending.

A truth that begins not in the balance sheet, but in the workshop where metal learns to become art.

📘 Banker’s Classification Table of Ornament Families (Gold Bar to Ornament)

How Different Gold Pieces Behave as Inventory, Collateral, and Risk

Ornament Family | PSU Banks | Private Banks | Regional Banks | SFBs | Cooperative Banks |

1. Plain Gold (22K) | ✔️ High | ✔️ High | ✔️ Very High | ⚠️ Moderate | ✔️ Very High (sometimes too high) |

2. Casting / Hollow Jewellery | ⚠️ Caution | ⚠️ Very Cautious | ⚠️ Mixed | ⚠️ Low | ⚠️/❌ Often overvalued |

3. Stone-Studded (CZ / Kundan / Diamond) | ❌ Accept gold weight only | ❌ Strict | ⚠️ Partial | ❌ Reject | ⚠️/❌ Often mis-funded |

4. Antique / Temple Jewellery | ❌ Avoid | ❌ Avoid | ⚠️ Cautious | ❌ Reject | ⚠️ Emotional overvaluation |

5. Filigree (Fine Work) | ❌ Avoid | ❌ Avoid | ⚠️ Limited | ❌ Reject | ⚠️ Risky |

6. Bridal Heavy Sets | ⚠️ Accept gold only | ⚠️ Strict | ✔️ Accept more due to local market | ⚠️/❌ Low | ⚠️/❌ Often over-valued |

7. Lightweight (18K/20K) | ⚠️ Purity check needed | ⚠️ Low comfort | ⚠️ Familiarity helps | ❌ Rarely accept | ⚠️ Often overvalued |

8. Coins & Bars | ✔️ Best | ✔️ Best | ✔️ Best | ✔️ Best | ✔️ Best |

9. Custom/MTO Pieces | ❌ Avoid | ❌ Avoid | ⚠️ Accept limited | ❌ Reject | ⚠️ Often accepted (risky) |

10. Old Gold / Exchange Stock | ⚠️/❌ Reject | ❌ Reject | ⚠️ Partial | ❌ Reject | ⚠️ Accept (dangerous) |

11. Principal Gold (Job-Work Gold) | ⛔ Exclude | ⛔ Exclude | ⛔ Exclude | ⛔ Exclude | ⚠️ Sometimes wrongly included |

© Vivek Krishnan | The Vivek Perspective | 2025 | |||||

🔍 What this table helps a banker see

Not all “jewellery stock” behaves like gold.

Some categories behave like bullion → ideal for collateral.

Some categories behave like fashion inventory → worthless for collateral.

Some categories belong to someone else (principal gold) → should be fully eliminated from stock statements.

This is where the banker–karigar gap becomes clear:

Karigars know which items melt cleanly, crack easily, retain weight, or lose wastage. Bankers often treat all stock as equal grams — a dangerous assumption.

❌ The “Conversion Ratio Margin” Myth — And Why It Has Zero Value

In wholesale jewellery and job-work business models, it is common to hear:

“Sir, we keep 4–6% of gold during conversion.That retained gold is our equity, our margin.”

It sounds attractive. It even sounds logical. But for a banker, this has no value.

Here’s why.

🔍 1. It is not equity. It is merely unreturned principal gold

When a wholesaler or principal gives 1 kg of gold to a job-worker, and the job-worker returns 950–960 grams after manufacturing:

The missing 40–50 grams is claimed as “retained gold”

The business team pitches this as “margin” or “skin in the game”

But in reality:

This is not money the borrower has invested.This is gold the principal has lost or allowed due to process wastage.

It is not promoter contribution. It is not collateral. It is not equity. It is simply process shrinkage.

🔍 2. The retained grams are already “priced in” — not an extra buffer

Wholesalers build wastage into:

making charges

purity margins

design premiums

merchant commissions

Meaning: the margin is embedded in the transaction, not in the borrower’s balance sheet.

There is nothing extra available to form “equity”.

🔍 3. This gold is not owned by the job-worker

Ownership is the key principle in credit.

The job-worker does not:

pay cash for this gold

take price risk

have the right to liquidate it independently

If a jeweller cannot sell that retained gold without violating the principal–worker relationship, it is not his collateral.

Ownership ≠ possession. Bankers must recognise this difference.

🔍 4. In most audits, this “margin” cannot be traced

Ask any auditor or stock verifier:

Where is this “retained” gold recorded?

In which ledger does it sit?

Under what heading?

Is purity verified?

Answer: It is never clearly documented.

Because it is not a real asset. It is an accounting assumption framed by the industry.

🔍 5. It creates a dangerous illusion of comfort for lenders

When business teams pitch:

“Sir, borrower has 4–6% natural margin; GML is safe.”

…they forget that this “margin”:

Is not cash

Is not bankable

Does not cover price volatility

Cannot repay interest

Cannot be pledged

Does not show up in net worth

So in stress situations, this margin evaporates first…and the GML gap widens fastest.

🚨 The Banker’s Bottom Line

Process wastage is NOT equity. Retained gold is NOT promoter margin. Job-work leftover grams are NOT collateral.

Any lending structure that assumes this “conversion margin” is a buffer is fundamentally flawed.

If GML goes wrong, this so-called buffer:

cannot be seized

cannot be melted

cannot be auctioned

cannot be valued

cannot be enforced legally

It simply does not exist.

4. The Ornament Takes Life

From this point onward, gold stops being metal and becomes emotion:

A chain for a birthday

A bangle for a wedding

A necklace for a festival

A pair of studs for a child’s first gift

At every stage, value changes:

Metal value

Labour value

Design value

Stone value (if any)

Sentimental value

And these values behave differently in a banker’s world.

Some ornaments melt beautifully into pure gold. Some lose too much in wastage. Some are impossible to value without dismantling. Some contain gold that does not belong to the jeweller (principal gold).Some have stones worth nothing in liquidation.

This is why stock statements lie, unless the banker understands the journey.

🌟 Why This Journey Matters to a Banker

Because every gold loan, every CC limit, every WCTL, every GML, and every takeover proposal is built on one assumption:

“The gold shown in the stock actually exists and behaves predictably.”

But gold never behaves uniformly.

Its behaviour depends on:

Purity

Manufacturing method

Ornament family

Labour intensity

Stone content

Melt loss

Whether the gold actually belongs to the borrower

Understanding the journey of a gold bar is the only way to understand:

Collateral risk

GML stress

Conversion myths

Wastage manipulation

Stock overstatement

Bullion vs ornament behaviour

A banker who knows how gold travels will never be misled by how gold appears.

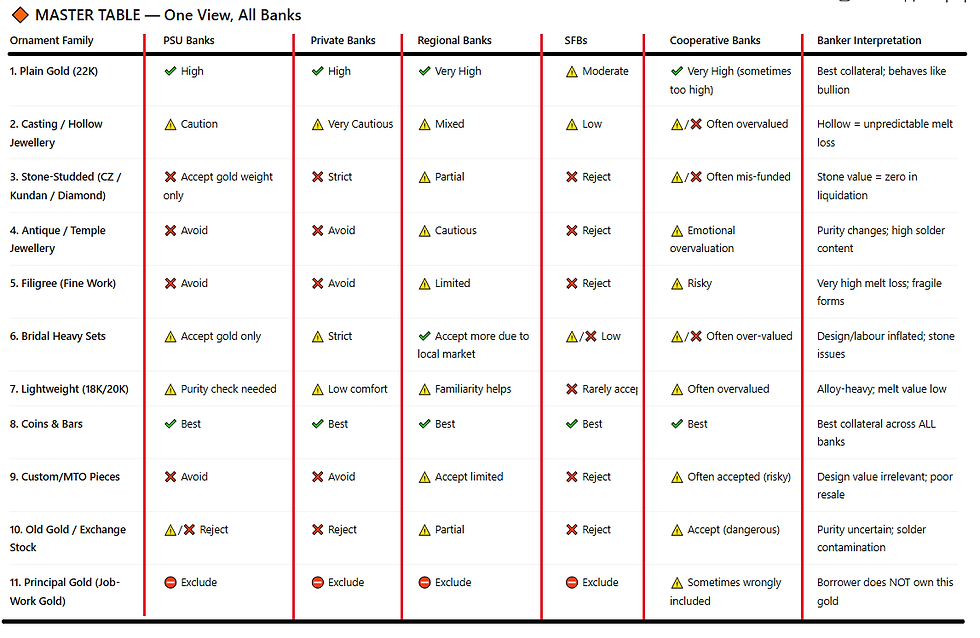

📘 Unified Banker Table: Ornament Family vs Bank Type Funding Comfort

Legend:✔️ High Comfort | ⚠️ Caution | ❌ Avoid | ⛔ Exclude Entirely

🔶 MASTER TABLE — One View, All Banks

Ornament Family | PSU Banks | Private Banks | Regional Banks | SFBs | Cooperative Banks | Banker Interpretation | |

1. Plain Gold (22K) | ✔️ High | ✔️ High | ✔️ Very High | ⚠️ Moderate | ✔️ Very High (sometimes too high) | Best collateral; behaves like bullion | |

2. Casting / Hollow Jewellery | ⚠️ Caution | ⚠️ Very Cautious | ⚠️ Mixed | ⚠️ Low | ⚠️/❌ Often overvalued | Hollow = unpredictable melt loss | |

3. Stone-Studded (CZ / Kundan / Diamond) | ❌ Accept gold weight only | ❌ Strict | ⚠️ Partial | ❌ Reject | ⚠️/❌ Often mis-funded | Stone value = zero in liquidation | |

4. Antique / Temple Jewellery | ❌ Avoid | ❌ Avoid | ⚠️ Cautious | ❌ Reject | ⚠️ Emotional overvaluation | Purity changes; high solder content | |

5. Filigree (Fine Work) | ❌ Avoid | ❌ Avoid | ⚠️ Limited | ❌ Reject | ⚠️ Risky | Very high melt loss; fragile forms | |

6. Bridal Heavy Sets | ⚠️ Accept gold only | ⚠️ Strict | ✔️ Accept more due to local market | ⚠️/❌ Low | ⚠️/❌ Often over-valued | Design/labour inflated; stone issues | |

7. Lightweight (18K/20K) | ⚠️ Purity check needed | ⚠️ Low comfort | ⚠️ Familiarity helps | ❌ Rarely accept | ⚠️ Often overvalued | Alloy-heavy; melt value low | |

8. Coins & Bars | ✔️ Best | ✔️ Best | ✔️ Best | ✔️ Best | ✔️ Best | Best collateral across ALL banks | |

9. Custom/MTO Pieces | ❌ Avoid | ❌ Avoid | ⚠️ Accept limited | ❌ Reject | ⚠️ Often accepted (risky) | Design value irrelevant; poor resale | |

10. Old Gold / Exchange Stock | ⚠️/❌ Reject | ❌ Reject | ⚠️ Partial | ❌ Reject | ⚠️ Accept (dangerous) | Purity uncertain; solder contamination | |

11. Principal Gold (Job-Work Gold) | ⛔ Exclude | ⛔ Exclude | ⛔ Exclude | ⛔ Exclude | ⚠️ Sometimes wrongly included | ||

© Vivek Krishnan | The Vivek Perspective | 2025 |

⭐Summary in One Line per Bank Type

PSU Banks → Very structured, avoid design-heavy items, follow melt value strictly

Private Banks → “Scientific lenders” — purity, density, hallmarking, documentation

Regional Banks → Relationship-driven, strong understanding of local jeweller markets

SFBs → Very low comfort with ornaments; prefer coins/bars or plain 22K items

Cooperative Banks → Trust-based lending, often overvalue stock → major risk hotspot

🟦 Banker’s DO & DON’T Quick Reference Sheet for Jewellery Lending

✅ BANKER DOs —

What You Must Do

When Funding Jewellers

1. Do prioritise Plain Gold (22K) as collateral

Most predictable melt behaviour

Lowest wastage variance

Easiest to value and liquidate

Highest comfort across all bank types

2. Do accept Coins & Bars with maximum DP

True near-bullion asset

Minimal ambiguity

Best form of security

3. Do segregate stock clearly into ornament families

Plain gold

Casting

Stone-studded

Filigree

Bridal

Job-work

Old gold Each behaves differently in stress.

4. Do verify purity scientifically

Hallmarking is NOT enough

XRF testing + random melt test

Prevents 18K being presented as 22K

5. Do insist on proof of ownership

Especially for:

Principal gold

Job-work gold

Memo/consignment pieces

Borrower must own the gold they pledge.

6. Do apply differentiated haircuts per ornament family

Coins/bars → Highest DP

Plain gold → Stable DP

Casting → Higher haircut

Filigree/Stone → Deep haircut or reject

Job-work → Exclude

Old gold → Accept only melt value

7. Do track inventory turnover

High-turnover jewellers behave differently from slow-moving showrooms. Turnover tells the truth.

8. Do visit the workshop

The workshop reveals:

Purity practices

Karigar quality

Stock movement

Whether the metal behaves as per books

9. Do reconcile gold issued vs gold returned

Any mismatch indicates:

Stock inflation

Wastage manipulation

Double financing

Cannibalisation of GML

10. Do understand the local market

Temple jewellery in TN ≠ Filigree in Odisha ≠ Casting in Gujarat. Collateral behaviour is geographical.

❌ BANKER DON’Ts — What You Must Never Do When Funding Jewellers

1. Don’t treat all jewellery as equal grams

A 100g plain bangle ≠ a 100g stone necklace.

2. Don’t accept stone value

Diamonds, CZ, Kundan — all melt to zero. Accept only gold weight.

3. Don’t accept Job-Work / Principal Gold as security

Borrower doesn’t own it. Zero collateral value. Zero.

4. Don’t fund based on invoice value

Invoices contain:

Labour

Design

Stone

Making charges

All of which have zero value during liquidation.

5. Don’t accept filigree or hollow items at full value

Melt loss is very high. Weight ≠ purity.

6. Don’t rely only on hallmark stamps

Hallmarking frauds are common. Always test purity.

7. Don’t ignore old gold in the stock statement

Old gold = solder contamination = purity uncertainty. Treat with suspicion → deeper haircuts.

8. Don’t allow conversion ratio to be pitched as “margin”

Wastage ≠ equity. Retained gold ≠ promoter contribution.

9. Don’t fund inventory that doesn’t move

Slow-moving stock = liquidity trap. Liquidation value collapses.

10. Don’t accept jewellery as collateral without understanding melt behaviour

The furnace tells the truth — not the invoice, not the showcase.

⭐ One-line mantra for bankers

A jeweller’s stock is art for the customer, inventory for the merchant, but collateral only for the banker who understands how it melts.

🔒 Disclaimer

The insights, classifications, and frameworks presented in this article are based on the author’s personal engagements, discussions, and interactions with a wide range of experts in jewellery manufacturing, gold appraisal, bullion trading, credit underwriting, and risk management. These conversations, along with the author’s professional experiences, have been interpreted, organised, and articulated here purely for educational, informational, and reference purposes.

The views expressed are entirely personal to the author. They do not represent the official position, policy, or guidance of any institution, employer, or industry body, nor should they be regarded as professional, financial, or legal advice.

Readers are advised to exercise their own judgment and seek professional guidance wherever required.

All content, including text, tables, classifications, and explanations, is intellectual property of the author. Reproduction, redistribution, or adaptation of any material from this article requires explicit written permission from the author.

Comments