March is the most sensitive month in the books of any bank.

As the financial year closes, the quality of the loan portfolio — especially SMA accounts and NPAs — comes under intense scrutiny.

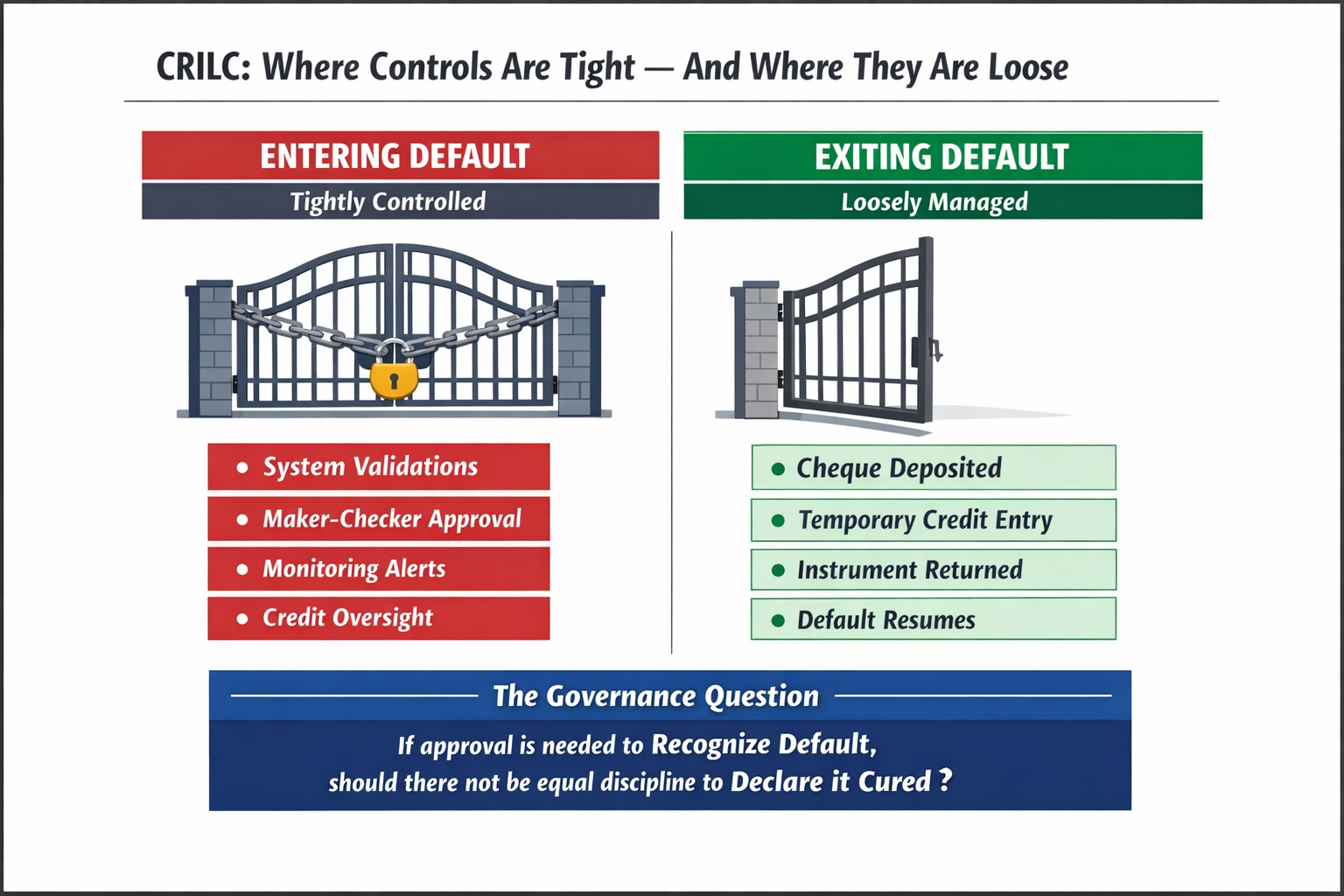

To strengthen early detection of stress in the banking system, the Reserve Bank of India introduced the CRILC framework — the Central Repository of Information on Large Credits.

The objective was simple but powerful.

Create a system where banks report early signs of borrower stress so that emerging risks are visible across the financial system.

What CRILC Framework Was Designed to Capture

Under this framework, borrower accounts are categorized based on days past due:

SMA-0: 1–30 days overdue

SMA-1: 31–60 days overdue

SMA-2: 61–90 days overdue

Once an account crosses 90 days past due, it is classified as an NPA.

The idea is to create a structured early warning ladder so that lenders do not discover stress only when an account has already deteriorated.

CRILC therefore acts as a system-wide early warning system.

How Systems Operationalize This

In most banks today, these classifications are determined automatically through system logic based on overdue positions at the end of each day.

When an overdue is cleared through actual repayment, the account moves out of delinquency.

When the overdue persists, the system moves the account progressively through the SMA stages.

In theory, this framework should ensure that repayment behaviour and risk recognition remain aligned.

Where Behaviour and Systems Diverge

However, operational systems sometimes reveal an interesting asymmetry.

Moving an account into default usually involves controls:

validations

monitoring alerts

internal oversight.

But moving an account out of default can sometimes be triggered by something as simple as a transaction entry.

A cheque is deposited.

The system temporarily reflects a credit.

The account appears to move out of delinquency.

A few days later, if the cheque is returned unpaid, the reversal is posted and the account slips back again.

If such transaction cycles occur during the SMA monitoring period, the account may appear to exit and re-enter delinquency multiple times without any real repayment taking place.

The borrower has not paid.

Yet the system briefly believes repayment has happened.

The Governance Question

The issue here is not about cheques.

It is about control symmetry.

If institutions require governance and approvals to recognize default, should there not be equal discipline around declaring that default has been cured?

Because credit risk is determined not by transaction activity, but by actual repayment behaviour.

The CRILC Paradox

The CRILC framework was introduced precisely to improve transparency and early detection of stress.

Yet within many institutions, the internal processes around SMA monitoring, curing events and reporting remain something of a black box.

Which is why, as March approaches each year, the old warning still feels relevant.

Not about emperors.

But about balance sheets.

Beware the Ides of March.

Archive note

This essay was restored from Vivek Krishnan’s Wix journal. Its original wording and available visuals have been preserved.

This page is now the permanent canonical edition within Vivek Perspective.