From Paperless Lending to Intelligent Lending

- 2 hours ago

- 6 min read

Episode 1: The Hidden Waste in Lending

A Lean View of Why Paper Is Only the Visible Problem.

For many lenders, transformation has been described in terms of digitisation.

Paper forms became PDFs. Physical files became digital folders. Branch workflows moved into loan origination systems. Dashboards replaced printed MIS. Customer communication moved from letters to SMS, WhatsApp and email.

This was necessary. But it is not sufficient.

The next stage of transformation in lending will not be defined by whether a document is digital. It will be defined by whether the institution can understand what the document says, what risk it carries, what exception it reveals, what action it should trigger and what should still be left to human judgement.

That is the shift from paperless lending to intelligent lending.

This distinction is particularly important particularly for relationship-led NBFCs or FIs / Banks. Their strength has never been technology alone. It has been trust, local market knowledge, long-standing customer relationships, field intelligence and the ability to understand small entrepreneurs, vehicle owners and self-employed customers beyond numbers.

For such institutions, AI should not sit in front of the customer as a cold replacement for human interaction.

AI should sit behind the frontline and make the frontline stronger.

The Visible and Invisible Waste in Lending

The most visible waste in lending is paper.

Printing, stationery, photocopies, physical files, scanned documents, courier movement and repeated documentation are easy to see. They appear as administrative cost. They are visible in budgets. They are easy to complain about.

But paper is only the visible symptom.

Behind it lies a much larger institutional waste:

The most expensive wastage in lending is not paper.

It is human attention being spent on work that systems should support.

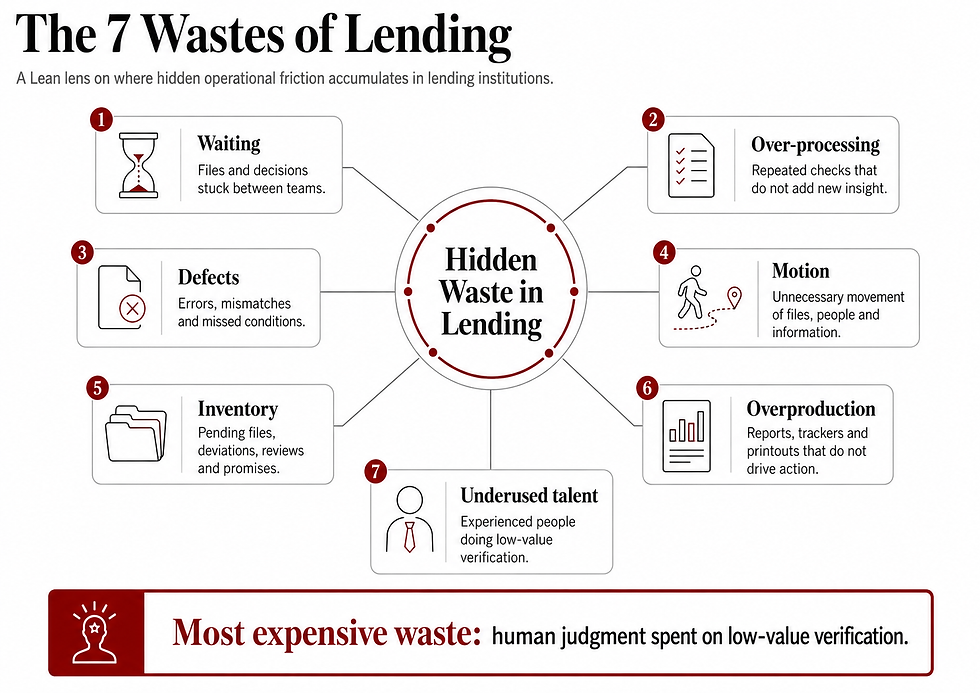

The 7 Wastes of Lending

The classic Lean framework can be adapted into a practical model for financial services.

I call this model the 7 Wastes of Lending.

The 7 Wastes of Lending model helps institutions look beyond paper and identify where real friction sits — waiting, repeated checks, errors, unnecessary movement, pending items, report overload and underused talent. Digitisation alone does not remove these wastes; it may only convert a physical file into a digital file with the same delays, rework and manual verification.

The better approach is to first identify where waste is weakening speed, control and judgement, and then use AI selectively to read documents, flag mismatches, summarise information, detect early warning signals and prioritise attention. The real transformation is from manual checking to exception-led review, where systems handle routine comparison and experienced people focus on exceptions and risk judgement. Paperless lending removes the file; intelligent lending removes the friction.

In credit origination, digitisation and analytics reduce the time relationship managers and credit officers spend on repetitive preparation and routine processing. This allows them to focus more on customer engagement, risk interpretation and better-informed decisions.

In loan operations, the same issue appears after sanction. Manual data entry, fragmented systems, multiple handoffs, reconciliation breaks and servicing backlogs consume skilled operations capacity. Experienced professionals who should be focused on quality assurance, exception handling and control are often pulled into mundane reconciliation and manual verification.

The implication is clear: the deepest waste in lending is not paper. It is expert capacity trapped in routine processing.

A modern lending institution must therefore redesign the full lifecycle — origination, underwriting, documentation, disbursement, servicing, monitoring and collections — around one principle: systems should handle routine preparation, comparison and routing; humans should handle judgement, exceptions and relationship-sensitive decisions.

The CAM as Hidden Waste

The Credit Assessment Memo is a good example of hidden waste in lending.

In many institutions, analysts fill large volumes of information across multiple sheets and sections. Business profile, financials, banking conduct, collateral, deviations, market feedback, risks, mitigants and recommendations often repeat the same facts in different forms.

This creates two problems.

First, it consumes experienced analyst time in data placement, formatting, cross-referencing and repetition.

Second, it creates a communication risk. The same fact, if presented differently in different sections, can weaken the reader’s confidence in the quality of underwriting.

A weakly worded CAM does not automatically mean the assessment is weak. But it creates doubt about whether the assessment was complete, connected and consciously reasoned.

The CAM is not the assessment. It is the institution’s evidence that assessment has happened.

A good CAM should therefore not merely compile information. It should connect facts, interpret risk, explain mitigants, acknowledge weaknesses and show why the recommendation is still bankable.

This is where human judgement matters most.

But if analysts spend most of their time filling sheets, copying information, reconciling repeated data points and correcting language, then judgement is trapped in documentation mechanics.

The opportunity is not to let AI write credit decisions.

The opportunity is to let AI support consistency, completeness and clarity — so that credit officers can focus on the real question: does the borrower deserve the risk?

A good system should separate three layers:

Data quality: Are numbers, names, dates, limits, securities and conduct details correct?Credit logic: Does the assessment connect business, financials, conduct, risks and mitigants?Credit communication: Does the CAM clearly explain why the proposal is acceptable or not?

A CAM with too many errors is not merely an analyst problem. It may indicate a system problem across time, workload, review design, role clarity, templates, training, supervision bandwidth and quality gates.

This is exactly a Lean Six Sigma point. In a mature process, defects should be detected close to the point of origin. If a defect travels through multiple levels and reaches the top most head, it means the quality gate failed.

But a failed quality gate does not mean every gatekeeper is incompetent. It may mean:

The analyst had insufficient time.

The CAM format encouraged repetition and inconsistency.

The supervisor reviewed for credit substance, not data consistency.

The checklist was too broad and mechanical.

The same information was scattered across too many places.

The review hierarchy lacked clear ownership.

The system did not highlight mismatches.

The culture rewarded speed of movement over quality of preparation.

The Relationship-Led Financial Institution Context

This is especially important for relationship-led NBFCs / FIs.

Their advantage lies in trust, local knowledge, customer proximity and field understanding.

Many of their customers are small entrepreneurs, vehicle owners, traders and self-employed individuals. Such customers cannot always be understood only through formal data.

A bureau score may not explain seasonality.

A bank statement may not fully explain business resilience.

A delay may not always indicate wilful default.

A clean document may not always indicate low risk.

Human judgement matters.

But human judgement should be used where it adds value.

A field officer should spend more time understanding the customer, not feeding the system.

A credit officer should spend more time interpreting business risk, not chasing papers.

An operations officer should spend more time handling exceptions, not manually searching for routine mismatches.

A collections officer should spend more time understanding borrower behaviour, not calling without context.

In such institutions, AI should not sit in front of the customer as a replacement for the relationship.

It should sit behind the frontline and make the frontline stronger.

The Leadership Implication

For leaders, the first step in AI-led transformation is not to announce AI pilots.

The first step is to identify waste.

Where is waiting highest?

Where is rework repeated?

Where are defects recurring?

Where are files moving unnecessarily?

Where are pending items accumulating?

Where are dashboards producing noise?

Where is talent underused?

Only after this diagnosis should the institution decide where AI, automation, workflow redesign or policy simplification is required.

This is where Lean and AI can work together.

Lean tells us what to remove.

AI helps us detect, compare, summarise, prioritise and learn.

But leadership must ensure that AI does not automate a weak process without questioning it.

The right sequence is:

Map the waste--> Redesign the process.--> Apply technology where it helps. --> Build controls around it.-- >Measure outcomes. ---> Improve continuously.

That is the path from paperless lending to intelligent lending.

The Doorman Fallacy in Lending

One of the hidden traps in lending operations is the doorman fallacy — the assumption that because a task keeps people busy, the task must be valuable.

In many lending processes, experienced people spend time checking repeated fields, reconciling documents, correcting CAM language, following up for clarifications, preparing trackers and reviewing information already available elsewhere. The work is real. The effort is real. But the value created by that effort may be limited.

This is where leaders must distinguish between necessary judgement and avoidable process labour.

A credit officer interpreting borrower risk is creating value. A credit officer repeatedly matching the same data across multiple sheets is often compensating for poor process design.

The question is not whether people are working hard.

The question is whether the process deserves their judgement.

AI, workflow redesign and Lean thinking should therefore not be used merely to make the doorman faster. They should ask whether the door itself needs redesign.

In lending, transformation begins when we stop glorifying manual friction as diligence.

Summary :

Paperless lending removes visible waste, but intelligent lending must remove hidden waste — waiting, rework, repeated checking, late exceptions, dashboard noise and underused human judgement.

AI becomes meaningful only when it frees people from low-value verification and allows them to do what only people can do: understand context, assess intent, interpret risk and make responsible credit decisions.

Comments